Навигация

Poland and Hungary as the best example of transition in the East Europe

66947

знаков

3

таблицы

1

изображение

2.2. Poland and Hungary as the best example of transition in the East Europe

Economic Reform in Eastern Europe: The Background

The background of economic reform in Eastern Europe is not unlike that in the Soviet Union, even though, as I have emphasized, the setting is rather different. The brief political thaw following the death of Stalin in the early 1950s did permit a freer discussion of ideas, which, along with growing problems of economic performance, led to limited attempts to develop and implement economic reform. Initially, these changes were modest in scope, and they typically followed the Soviet reform pattern: Try to improve decision making while preserving socialist objectives and the essence of the planning system. This was the focus of the New Economic System in the GDR and of the New Economic Mechanism introduced in Hungary in 1968. The potential for genuine economic reform was certainly limited by Soviet influence. Indeed in some cases (such as Czechoslovakia in 1968), reform was abruptly forestalled by Soviet intervention. In other cases, such as Hungary, reform attempts dating from the late 1960s were sustained on a limited basis, to become the background for more serious reform in the present era. There were, then, numerous attempts at reform in Eastern Europe. What were the major forces promoting these efforts?

First, as was the case in the Soviet Union, rates of economic growth in Eastern Europe have undergone a long-term secular decline. The magnitude of this decline (see Table 1) has varied from case to case, but overall it has been pervasive. Moreover, these countries had taken pride in being high-growth economies, even if the costs, such as little growth of consumer well-being, were also high. At the same time, growth in productivity slackened, especially in the late 1970s and 1980s. And inflation quickened, though it was most serious in Poland and Yugoslavia. Repressed inflation, though difficult to measure, grew in importance in the 1980s.

Second, East European countries relied heavily on foreign trade as a means of stimulating economic growth in the 1970s. Their strategy was to promote exports in Western markets so that the imports required both to stimulate technological change in industry and to enhance consumer well-being could be obtained without the growth of hard-currency debt. Unfortunately, this strategy was not successful. The energy crisis led to a significant slackening of Western markets at the very time when East European nations were becoming more aggressive in these markets. East European imports were sustained, but largely by means of building a substantial hard-currency debt. The magnitude of debt repayment subsequently led to considerable internal belt-tightening for these countries in the 1980s — precisely the opposite of what had been intended.

Third, one could argue that in Eastern Europe, the possibilities for economic growth through extensive means had initially been less promising than in the Soviet case and had been exhausted more quickly. In light of the level of economic development in Eastern Europe compared to that in the Soviet Union, it is not surprising that the imperative for reform was strong and that developments of the Gorbachev era quickly spilled over into Eastern Europe. In the absence of Soviet backing, interest in the administrative command model faded fast.

Table 1. Economic Growth and Performance in Eastern Europe:

The Background to Reform

| 1961-70 | 1971-80 | 1981-85 | 1985 | 1986 | |

| Eastern Europe | 3.4 | 2.4 | 1.0 | .2 | 2.2 |

| Bulgaria | 5.0 | 2.3 | .1 | -3.2 | 4.7 |

| Czechoslovakia | 2.4 | 2.3 | 1.0 | .4 | 1.9 |

| East Germany | 3.2 | 3.5 | 1.7 | 3.3 | 1.6 |

| Hungary | 3.1 | 2.5 | .6 | -2.3 | 2.4 |

| Poland | 3.3 | 3.0 | 1.0 | .2 | 2.1 |

| Romania | 4.2 | 3.5 | -.6 | -1.4 | 3.1 |

East European Reform Programs: Similarities and Differences

In this chapter we pay special attention to Poland and Hungary. We do so because these countries are both examples of aggressive reform but have employed different strategies. However, before we consider these cases in greater detail, it is useful to summarize the East European reform experience, noting important similarities and differences among the various cases. To do so will entail some repetition of basic themes.

First, economic reform in Eastern Europe (at least in Poland, Hungary, and Czechoslovakia) is generally described as a transition in that these countries seek to replace the planned economy with a market economy rather than attempting merely to modify the former.

Second, transition programs have varied in speed and intensity. Some countries have pursued reform on a "gradual" basis, whereas others, like Poland, have pursued what is often termed a "big bang," or rapid, approach to reform. However, we must remember that even in those countries not pursuing a "big bang" or "shock therapy" approach, the process of transition in Eastern Europe has been relatively rapid, especially when compared to reforms of the past - and notably so when compared to the recent Soviet record. It is important, therefore, to be aware of the basic issues associated with transition and of the extent to which the attempted speed of transition alters the overall reform experience.

Third, although it is possible to examine and understand the basic elements of economic reform and even of transition from one system to another, we really do not have a general theory of change in economic systems. In some cases — for example, during such a period of rapid change as the 1990s — it is difficult even to develop a way to classify the issues involved in transition.

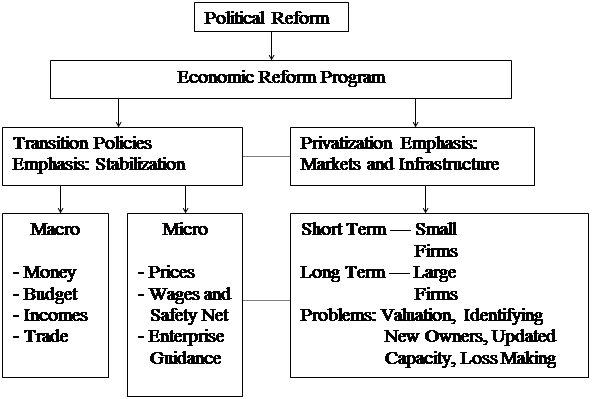

Fourth, important differences exist from one country to another. Our view of the socialist transition process is heavily influenced by our image of the best-known and most advanced reforms, such as those of Poland, Hungary, and Czechoslovakia. We know much less about, and tend to pay less attention to developments where reforms are proceeding at a slower pace, as in Romania and Bulgaria. Figure 1 offers a simple, stylized view of contemporary political and economic reform (transition) in Eastern Europe.

Figure 1. Reform in Eastern Europe

POLAND: FROM PLAN TO MARKET VIA SHOCK THERAPY

Until Solidarity won the parliamentary elections in Poland in the summer of 1989, the Polish economy had been, since the end of World War II, a rather typical planned socialist economic system. State ownership predominated, and though economic reform was attempted in varying degrees at different times, little real systemic change had taken place. Moreover, as Table 1 shows, the rate of economic growth continued to decline, and the period saw recurring shortages, increasing inflation, and an understandably declining work ethic.

Beginning in 1990, Poland took decisive steps toward a market economy. This "shock therapy" approach was to be sudden, and in this it differed significantly from the gradualist approach being discussed in other socialist systems. In addition to treeing prices, Poland implemented monetary controls, the zloty was made convertible into hard currencies, and steps were taken to control wage increases.

As we shall see, the "shock therapy" approach has not been without critics. Moreover, although the Polish case quickly attracted the interest of those who study the problems of socialist transition, it was viewed as unique. Thus it was argued that. for a variety of reasons that were discussed earlier, reform was much more likely to succeed in Poland than in a case like the Soviet Union. But before we examine the Polish reform experience in greater detail, we must review what brought the Polish economy to the reform phase and how, at that point, it might be different from other socialist countries.

I begin our discussion of Poland with a brief examination of the setting. Then I discuss the Polish command system, considering the extent to which this system led to distortions in the Polish economic structure. Finally, I turn to the issue of transition and examine the mechanisms utilized and the results achieved thus far.

1) Poland: The Setting

By European standards, Poland is a relatively large country. With a land area of just over 300,000 square kilometers, it is just over half the size of France. Moreover, with a population that approached 38 million in 1990, Poland is some 68 percent of the size of France in terms of population.

Poland is frequently viewed as having a homogeneous society, a factor that facilitates economic reform. Although social homogeneity is difficult to measure and may well be overstated in the Polish case and in other cases (for example, there are regional differentials, urban-rural differentials, and the like), the basic statistical evidence is strong. In terms of religion, 95 percent of the Polish population is Roman Catholic. From a stannic standpoint, 98.7 percent of the population is Polish, and only a few minority groups occur.

Urbanization and industrialization have changed the nature of Polish life and customs, but the church, family, and folk ties that have sustained Poland for a long time remain strong. Thus, although Poland must deal with problems of modernization, it also has valued traditions and a clear identity. These qualities make implementing change more manageable here than in many other countries.

In terms of natural resources, Poland is a country of considerable regional diversity, though major portions of the land area are not especially fertile.

Poland's main energy resource is coal; basic minerals and some deposits of oil and natural gas also exist. Both basic data and methods of computing economic aggregates of socialist systems are currently under scrutiny. New evidence that will make it possible to do different kinds of computations may well lead to important adjustments. With these reservations in mind, however, we note that Poland was reported to have a per capita gross national product of approximately $4500 measured in 1989 U.S. dollars. This figure places it between the high-income countries of the region (Hungary and Czechoslovakia) and the low-income countries (Bulgaria, Romania, Yugoslavia) and at one-quarter that of the United States. Prior to the onset of major economic reform, the bulk of Polish industry was state-owned and planned. Agriculture (representing roughly one-fifth of total Polish output) was a mixed system wherein the private sector produced about three-quarters of the total agricultural product. Foreign trade turnover — that is, exports plus imports — represents roughly one-third of Polish product, again using U.S. dollar measures.

2) Poland: The Command Economy

The organizational arrangements of the Polish command economy were established immediately after World War II and closely resembled those prevailing in the Soviet Union. There was widespread nationalization of property, central planning mechanisms were established, and agriculture was socialized. In addition to organizational arrangements, Polish economic policies of the era, such as those on investment, sectoral development, and the like, closely mirrored the Soviet model.

Although Poland attempted modification of the command system as early as 1956 when collectivization was abandoned, little actually changed. Over time, private agriculture was neglected by the state, and continuing political protests, especially in the early 1970s, signaled both political and economic difficulties.

The 1970s was a difficult decade for many countries, especially those that rely on imported oil. The Polish strategy in the 1970s and later was to stimulate the domestic economy through the importation of foreign technology. This was not an unreasonable strategy in theory, but Western economies were themselves in the midst of the energy crisis and the recession it caused. Poland's effort to expand exports failed, hard-currency debt accumulated, and the projected impact of Western technology on the Polish economy was minimal. As the 1970s came to an end, it was evident that domestic retrenchment would be essential — a difficult path in light of the continuing unrest among Polish workers. The 1980s began with roughly three years of martial law and an attempt to achieve economic stabilization.

After half-hearted economic reforms in the early 1980s, the rise of Solidarity (which had been outlawed in 1982) proved that major systemic and structural reform was necessary. Even so, and despite the fact that Polish economic performance was deteriorating badly, serious economic reform did not begin until the late 1980s.

3) The Polish Transition: The "Big Bang" in Practice

The Polish transition from plan to market has been watched closely by a variety of interested observers. Although many of the policy and systemic changes introduced in Poland are familiar hallmarks of the general reform scene, the speed of implementation in the Polish case is unique.

There had been attempts to decentralize decision making in large state-owned Polish enterprises in the 1980s, but these reforms failed to change outcomes (a possible exception is their contribution to the wage explosion that took place toward the end of the decade). Moreover, on the eve of reform in Poland (the reform program began officially on January 1, 1990), macroeco-nomic conditions there were in a state of severe disequilibrium. Although the exact nature of monetary overhang in Poland (as elsewhere) has been the subject of debate, there was a significant budget deficit, wage increases were out of control, and hyperinflation had resulted. Poland's hard-currency debt position was better than that of Hungary, but the debt that had been accumulated did little to stimulate the Polish economy, the zioty was overvalued, and no debt relief from external sources was in sight.

In the fall of 1989, most price controls were lifted (on both producer and consumer goods), public spending was reduced, and the zioty was devalued. In the second stage of major reform, begun in 1990, the budget deficit was sharply cut, largely through a reduction of subsidies to state enterprises. A positive real rate of interest was to be implemented, and the market was to be used to signal changes in the value of the zloty. The latter was a critical measure, because foreign trade and the impact of this trade on the Polish industrial structure was to be a key component of the overall reform strategy. In January of 1990, the government set the exchange rate of the zloty at 9500 to the dollar (this represented a devaluation from 1989), a rate roughly approximating its value on the black market, and it established convertibility of the zloty for international trade. Many trade restrictions were eliminated, and internal exchanges were set up to handle the buying and selling of hard currencies. Although these changes resulted in domestic inflation, the initial increases proved to be short-term and the exchange rate of the zloty has proved to be realistic.

Finally, wage increases were to be controlled partly through wage indexation and partly through a new tax on wage increases that exceeded established guidelines.

Privatization is a major element of the Polish strategy of transition. In 1990 the Polish government passed a law creating a Ministry of Ownership Change, a mechanism to supervise the process of privatization. Privatization has proceeded rapidly, though it has been achieved mainly for small enterprises in the trade and service sectors. Industrial output in the private sector grew by 8.5 percent in 1990 and is reported to represent roughly 17 percent of total Polish industrial output

Though privatization has been very successful for small-scale enterprises, the picture for large state enterprises is quite different. For reasons we noted earlier, privatization of these enterprises has proceeded very slowly. In addition, the economic position of these enterprises worsened as the state took decisive measures to introduce a hard-budget constraint. In addition to price changes and wage limitations, subsidies have been ended and protection from foreign competition has been sharply reduced. This new setting has encouraged enterprise managers to reduce costs by restricting unnecessary output and reducing the labor force. However, the strong commitment to rapid privatization was reinforced in June of 1991, when it was announced that a major portion of state industry would be privatized through creation of stock funds, with the population receiving vouchers.

Beyond these changes in the state sector, new guidelines have been introduced to monitor enterprise performance. Furthermore, a new Industrial Restructuring Agency will consider how remaining state enterprises should be handled, to what extent privatization is possible, and what restructuring should take place for those enterprises that are not viable in the new setting. These new arrangements are designed to ensure a rapid transformation of the Polish industrial structure, to make it similar to and competitive with market economic systems, and to achieve this result quickly and as openly as possible.

Note that these comprehensive reforms in Poland cover all the critical areas discussed in Chapter 4 and earlier in this chapter. Moreover, beginning from very precarious economic circumstance in 1989, these changes were introduced simultaneously and rapidly. We will now do our best to assess the early results.

4) The Polish Economy in the 1990s

It is clear that economic reform in Poland has been radical and has moved sharply and swiftly away from the plan toward the market. In addition to the expanded influence of market mechanisms, decision making has been decentralized, private property introduced, and incentive arrangements changed. By most standards, the initial results have been encouraging.

First, stabilization measures cut the rate of inflation sharply from a reported 40-50 percent per month at the end of 1989 to roughly 4-5 percent per month in 1990. At the same time output fell, though supplies of consumer goods in stores increased. Employment in industry declined by 20 percent during 1989 and 1990, although it is reported that only a relatively small portion of this reduction in the labor force was caused by forced layoffs. The unemployment rate was reported to be 6.5 percent at the end of 1990.

Another major positive facet of the Polish reform experience has been the foreign trade sector. There has been a significant expansion of exports, especially to hard-currency markets. This expansion resulted in part from the devaluation of the zloty to market-clearing levels and in part from the reorientation of trade away from the Soviet Union and other East European trading partners. At the same time, as a result of restrictive policy measures and the higher domestic cost of these imports, import demand declined.

A third qualified success has been privatization. Although the initial pace of privatization was rapid, this early privatization was largely that of small-scale enterprises in the area of trade and services. Although Polish reformers take seriously the need to pursue privatization of major state enterprises, bringing this about will remain a critical task for the next several years.

Can these achievements be sustained in the coming years? We discuss this issue more generally in the next section, but the Polish case deserves specific comment. Quite clearly, the continued success of the Polish transition will depend on the continuing implementation of appropriate stabilization measures. Although this may seem relatively straightforward, it requires cohesion and commitment among policy makers and willingness among the populace to pay the costs of the transition. Pressures for wage increases must be resisted, and the process of privatization must proceed. To the extent that the latter can be achieved, the contours of new market arrangements can be defined. Finally, although uncertainty in foreign markets remains, relief of hard-currency debt will unquestionably add a measure of flexibility.

Another issue is the extent to which the Polish "success" (if we can call it that) was promoted by Western assistance. In light of the Polish leadership's commitment to rapid transition, the West has provided considerable assistance in the form of exchange-rate stabilization funds, debt restructuring, and government guarantees.

HUNGARY: THE NEW ECONOMIC MECHANISM AND PRIVATIZATION

Early works in comparative economic systems devoted little attention to the Hungarian economy. Over the last twenty years, however. Western economists have begun to pay more attention to Hungary.

As one prominent observer of Hungary and other East European systems has noted, "The Hungarian reform experience says as much about central planning as it does about Hungary, and therefore an understanding of that experience is important for those interested in the prospects for reform in all of Eastern Europe, and indeed, in the Soviet Union. In other words, Hungary is a prototype of economic reform for the former planned socialist economic systems of Eastern Europe, and presumably elsewhere. These thoughts, expressed some ten years ago, remain relevant in the 1990s as Hungary, like other socialist systems, pursues a transition to the market. However, the background of reform in Hungary is important to a proper analysis of contemporary problems and prospects.

Prior to 1968, Hungary applied the Soviet model of centrally planned socialism in a typical fashion. But then, in 1968, Hungary began to introduce by far the most radical economic reform attempted in Eastern Europe (with the exception of Yugoslavia). In the words of one early observer of this reform, it clearly represents the most radical postwar change, in the economic system of any Comecon country, which has been maintained over a period of years and gives promise of continuity.

Although the reform program in Hungary met with only partial success, the problems that have arisen (conflicts of objectives, for example, and difficulty in persuading participants to change their ways) are fundamental to the reform experience of planned socialist systems.

Hungary shares many features with other Eastern and Southeastern European countries, such as Yugoslavia. It provides a refreshing contrast to the Soviet Union, which in some important respects is atypical. Hungary is a small country heavily dependent on foreign trade. The Hungarian experience with reforming foreign trade, and in particular its efforts to become integrated into the world economy both East and West, is prototypical. The difficulties of reforming the foreign trade mechanism arc crucial to the Hungarian economy as well as to the economies of many other systems of Eastern Europe.

1) Hungary: The Setting

Hungary is located in central Europe. Its land area of approximately 36,000 square miles makes it roughly the same size as the state of Indiana. Its population of about 11 million is comparable to that of the population of Illinois. Although Hungary is not self-sufficient in energy, it docs have supplies of coat, oil, and a number of minerals, including important bauxite deposits.

Although it has some rolling hills and low mountains, Hungary is basically a flat country with good agricultural land and a favorable climate. As in other East European countries, the period since World War II has seen the population flow from rural to urban areas and a changing balance of industrial and agricultural activity. Today, approximately half the population lives in urban areas.

Hungary is not particularly prosperous. Most estimates of its gross national product or per capita gross national product place Hungary in the middle of the East European countries. It is generally wealthier than Bulgaria and Yugoslavia and certainly wealthier than Albania; it ranks behind East Germany and Czechoslovakia. Hungary's per capita income appears to be close to that of Greece. In this sense, economic development remains a key issue in Hungary. By the standards of Western Europe, Hungary remains relatively poor; by the standards of the Third World, Hungary ranks among the more affluent countries.

2) The Hungarian Economy: Prereform

The postwar reconstruction of the Hungarian economy began quite modestly in 1945.Before the implementation of a three-year plan in 1947 (1947-1949), the main policies included stabilization of the currency, changes in the nature of rural landholdings, and the beginnings of nationalization. The first three-year plan was designed primarily to bring the economy up to prewar levels of economic activity. During this time, a planning mechanism was created and the share of national income going to investment increased sharply. The changes were not radical, however, and balanced development was envisioned.

The era of balanced development came to an end with the introduction of a five-year plan in 1950. The share of national income devoted to investment was increased substantially, and the bulk of new investment was directed toward heavy industry. This policy was partially reversed toward the end of the plan period, but it was reaffirmed in 1955-1956.

A number of economic trouble spots cried out for attention. There was an observed need to improve industrial labor productivity, especially through the development of a better incentive system to offset the declining supply of labor from rural areas. Supply-demand imbalances were growing increasingly severe. Waste and imbalance in the material-technical supply system created the need for a substantially modified coordinating mechanism among enterprises.

In addition, excess demand for investment led to substantial amounts of unfinished new construction and to the neglect of old facilities. Some mechanisms for the more rational allocation of capital investment had to be found. The adoption and diffusion of technological advances were seen as inadequate. Technological improvement was considered crucial for continued development of the economy.

This background seems familiar: a small country, the Soviet (Stalinist) model of industrialization, overcentralization, emphasis on extensive growth, rigidities of the plan mechanism, incentive problems, and the resulting difficulties. Against this background, the New Economic Mechanism first promulgated in a party resolution in 1966 was put into, practice in 1968. Over twenty years later, it remains one of the most important reform programs of planned socialist systems.

3) Intent of the New Economic Mechanism

There is disagreement about the importance and effect of the Hungarian reform program. The New Economic Mechanism (NEM) has generally been interpreted as leaving the power to control the main lines of economic activity (volume and direction of investment, consumption shares) with the central authorities, while relying on the market to execute the routine activities of the system. The NEM called for substantial decentralization of decision-making authority and responsibility from upper-level administrative agencies to the enterprise level. In a general way, NEM bears a close resemblance to the Lange model. Let us consider the original blueprint of NEM.

The objective of NEM was to combine the central manipulation of key variables with local responsibility for the remaining decisions. The first change was a significant reduction in the number and complexity of the directives firms; for large state-owned firms, the traditional problems remain. Valuation is difficult, especially in loss-making enterprises. Moreover, it is hard to find buyers for these types of enterprises, let alone to arbitrate the potential rights of past owners. And just as elsewhere, privatization in Hungary is likely to become slower and more difficult as the focus shifts to the less attractive, large enterprises.

In addition to privatization per se, Hungary has addressed the creation of infrastructure (for example, a stock market) and new rules designed to change the guidance of enterprises. Accounting procedures have been refined and bankruptcy laws strengthened so that state subsidies can be curtailed and hard budgets introduced into large state-owned enterprises.

Hungary has also pursued a variety of stabilization measures and has liberalized policies in the sphere of foreign trade, though to a lesser degree and certainly more gradually than Poland. Domestic price controls have been substantially removed, and enterprises are permitted to enter into and benefit from foreign trade transactions. Although there are limits on the holding of foreign exchange, the Hungarian forint is substantially convertible for business purposes. However, the Bank of Hungary has maintained controls such that it has access to foreign exchange earnings to serve as repayment of the Hungarian hard-currency debt. (Hungary has a per capita hard-currency debt roughly twice that of Poland). Hungary has followed a tight monetary policy designed to create a balanced budget and also to exert financial pressure on enterprises.

Hungary has very liberal laws regarding foreign investment, including the possibility of full foreign ownership with permission. Moreover, repatriation laws are liberal. Not surprisingly, Hungary has been considered a leader in the quest to attract foreign investment, though the magnitude of this investment and its overall impact on the Hungarian economy probably remain modest.

The initial results of the transition process in Hungary have generally been positive when judged against the sorts of expectations that we discussed earlier. At the same time, it is proving difficult to sustain popular support as the inevitable costs of the transition process take their toll.

4) The Hungarian Economy in the 1990s

In spite of a tendency to compare the processes of economic reform in Poland and Hungary, there are important differences between the two systems, and especially in the degree to which prior reform had taken place. Although some would argue that the New Economic Mechanism was quite limited compared to contemporary reforms, nevertheless the reform process has a significant history in Hungary. The differences between the Hungarian and Polish cases are important.

Inflation has been much less serious in Hungary than in Poland. The annual rate of inflation for 1989 has been estimated at roughly 17 percent. Although the inflation rate increased to about 29 percent in 1990, this performance has been viewed as positive. In addition, wage increases have generally been controlled. Largely because of a shift away from trade with former CMEA trading partners, the volume of Hungarian trade has declined. At the same time, the Hungarians have experienced growth in exports to Western markets and a generally weak domestic demand for imports — both important developments for the overall trade balance. The good news on the exports side, however, tends to be sector-specific. Hard-currency debt remains a serious problem, and the movement toward a convertible currency has been much slower than in the Polish case. Finally, the Hungarian budget deficit has increased.

The Hungarian economy was projected to shrink by approximately 3 percent in 1991, and associated declines in consumption and investment were anticipated. The state property agency is moving ahead with privatization. The overall relatively slow pace of reform in Hungary may well dictate less sharp downturns and less severe fluctuations during the periods of downturn but, at the same time, rather slower recoveries and a longer time in which to achieve normalization. As with Poland, the effectiveness of the macroeconomic policies being implemented, world market conditions (such as the price of oil), and domestic structural change through privatization will all affect both short-term and longer-term outcomes.

EASTERN EUROPE: THE REFORM SCENE

The transition from plan to market in Eastern Europe is important, not only for those who live with and implement the transition, but also for those interested in the subject of comparative economic systems. For a variety of reasons, if the transition cannot succeed in countries such as Poland and Hungary, it is unlikely to succeed elsewhere.

Obviously, it is too early to render any definitive judgment on these cases, let alone on the more general issues of transition. Indeed, it is difficult to chart even basic day-to-day changes in these countries. That having been said, let us try to assess the outcomes that have occurred so far.

Judged in terms of our earlier discussion of economic reform and projected outcomes in the early stages of transition from plan to market, there is room for guarded optimism as we examine the early results in Hungary and Poland. At the same time, there remain a number of basic forces that will heavily influence future economic trends.

First, although initial political transformations are substantially complete in Eastern Europe (with important exceptions such as Yugoslavia), there are cases (such as Romania) where political instability and a lack of cohesion (derived in part from the political legacy of the communist era) make agreement on reform very difficult. Clearly, in these cases, the path of reform will be slower and much more difficult than in the leading cases that we have examined.

Table 2. Political and Economic Developments in Eastern Europe: A Summary

| Status of | Country | ||||||

| Poland | Hungary | Czech and Slovak Federal Republic | Bulgaria | Romania | Albania | Yugoslavia | |

| Post Economic Reform | Limited efforts in the 1980s | Important: New Economic Mechanism since 1968 | Limited: ended by Soviet inter vention 1968 | Limited | None | None | Important Worker: management and market socialism |

| Per Capita GNP - 1989, in U.S. S | 4607 | 6303 | 7922 | 3610 | 3154 | n.a. | 3409 |

| Percent Change in GNP: 1989-90 | -8.9 | -3.6 | -3.2 | -3.6 | -11.3 | n.a. | -6.9 |

| Official Consumer Price Index in 1989, 1980 = 100 | 3387 | 276 | 120 | 363 | 186 | n.a. | 761175 |

| Real per Capita Disposable Income in 1989, 1980 = 100 | 116 | 115 | 115 | 126 | 121 | n.a. | 114 |

| Current Economic Reform | Aggressive pursuit of transition, privatization continues | Ambitious transition plan in progress: stabilization, privatization, and attention to trade | Transition pursued with caution; initial results not as good as in Poland but positive | Reform began in 1991; price flexibility, privatization, and trade reform | Modest reforms from 1991; price adjustment, some privatization, and foreign investment | 1990-91: Limited first steps; decentralization, some privatization, and restructuring | Political turmoil and an economy largely without guidance |

Second, the initial results of the transition have been generally as expected. In Table2 I summarize a number of useful indicators. As anticipated, in all cases there has been a downturn in output — occasionally a downturn of significant magnitude. Inflation has been very uneven and in some cases (such as Yugoslavia and pre-reform Poland) very rapid. However, post-reform inflation rates generally leave some room for optimism, especially in those cases where stabilization policies have been developed and applied.

Third, we have noted that initial privatization usually proceeded rather quickly but that, after the privatization of small firms (especially in the service sphere), the pace of change decreased significantly. This latter development reflects the onset of major difficulties: the private sector must now absorb large, state-owned, loss-making, and often technologically backward enterprises. The privatization of these firms presents serious problems, as does a setting where valuation is fraught with difficulties, buyers are hard to find, claims from the past must be handled, and contemporary management skills are wanting.

Fourth, although inflation and unemployment have necessitated a growing concern for safety-net measures of various types, there is also a sense that the availability of consumer goods and services has improved.

All of these considerations seem to support a measure of optimism about the eventual outcome of the transition process. At the same time, there are important dimensions where change must be sustained if the transition is to be successful. Stabilization policies must be maintained — a tall order in those cases where consumer patience is lacking. Privatization must proceed, and it must increasingly reflect the contours of new market arrangements, including the infrastructure required for markets to function effectively. These changes must be sustained even in the face of political dissension, consumer dissatisfaction and an uncertain international economic environment. These restraining forces will in large part dictate the pace and ultimate success or failure of the transition process.

Похожие работы

... on trucks and utility vehicles, while the automobile industries in other countries may focus on sport cars or compact vehicles. Greater specialization allows producers to take full advantage of economies of scale. Manufacturers can build large factories geared toward production of specialized inventories, rather than spending extra resources on factory equipment needed to produce a wide variety ...

... of commerce in the East. Slovenia needs to strengthen its ties with other eastern countries, such as Russia, in order to develop its trade partners. The transitioning countries can serve as a new market for the West as well as Slovenia. Furthermore, additional trade partners exist in the far east, which are currently not being considered. Many challenges face the transition countries as ...

... conflicts arising from immigration of Muslims in Western Europe. Because of all these associations, immigration has become an emotional political issue in many Western nations. Chapter 2. Immigration in Europe 2.1. France As of 2006, the French national institute of statistics INSEE estimated that 4.9 million foreign-born immigrants live in France (8% of the country's population): The ...

... car manufacturing world. On July 24 and July 31 of 1998, the European Commission and the Federal Trade Commission, respectively, approved the merger of Chrysler and Daimler-Benz Corporation, and appearance of Daimler-Chrysler. This merger is classified as a “horizontal merger.” In order to become the largest car-producing corporation in the world, Daimler-Chrysler has to acquire or merger ...

0 комментариев