Навигация

Presentation

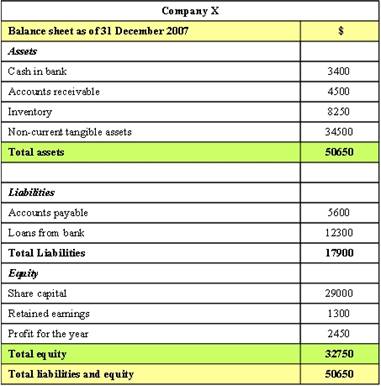

“Balance sheet”

1. Balance sheet

In financial accounting, a balance sheet or statement of financial position is a summary of a person's or organization's balances. Assets, liabilities and ownership equity are listed as of a specific date, such as the end of its financial year. A balance sheet is often described as a snapshot of a company's financial condition. Of the four basic financial statements, the balance sheet is the only statement which applies to a single point in time.

A company balance sheet has three parts: assets, liabilities and ownership equity. The main categories of assets are usually listed first and are followed by the liabilities. The difference between the assets and the liabilities is known as equity or the net assets or the net worth of the company; according to the accounting equation, net worth must equal assets minus liabilities.

Another way to look at the same equation is that assets equals liabilities plus net worth. This is how a balance sheet is presented, with assets in one section and liabilities and net worth in the other section. The sum of these two sections must be equal; they must "balance."

Records of the values of each account or line in the balance sheet are usually maintained using a system of accounting known as the double-entry bookkeeping system.

A business operating entirely in cash can measure its profits by withdrawing the entire bank balance at the end of the period, plus any cash in hand. However, real businesses are not paid immediately; they build up inventories of goods and they acquire buildings and equipment. In other words: businesses have assets and so they can not, even if they want to, immediately turn these into cash at the end of each period. Real businesses owe money to suppliers and to tax authorities, and the proprietors do not withdraw all their original capital and profits at the end of each period. In other words businesses also have liabilities.

A balance sheet, also known as a "statement of financial position", reveals a company's assets, liabilities and owners' equity (net worth). The balance sheet, together with the income statement and cash flow statement, make up the cornerstone of any company's financial statements. If you are a shareholder of a company, it is important that you understand how the balance sheet is structured, how to analyze it and how to read it.

2. Types of balance sheets

A balance sheet summarizes an organization or individual's assets, equity and liabilities at a specific point in time. Individuals and small businesses tend to have simple balance sheets. Larger businesses tend to have more complex balance sheets, and these are presented in the organization's annual report. Large businesses also may prepare balance sheets for segments of their businesses.

Personal balance sheet

A small business balance sheet lists current assets such as cash, accounts receivable, and inventory, fixed assets such as land, buildings, and equipment, intangible assets such as patents, and liabilities such as accounts payable, accrued expenses, and long-term debt. Contingent liabilities such as warranties are noted in the footnotes to the balance sheet. The small business's equity is the difference between total assets and total liabilities.

Corporate balance sheet

Guidelines for corporate balance sheets are given by the International Accounting Standards Committee and numerous country-specific organizations.

Balance sheet account names and usage depend on the organization's country and the type of organization. Government organizations do not generally follow standards established for individuals or businesses.

3. The Types of Assets

Current Assets

Current assets have a life span of one year or less, meaning they can be converted easily into cash. Such assets classes are: cash and cash equivalents, accounts receivable and inventory. Cash, the most fundamental of current assets, also includes non-restricted bank accounts and checks. Cash equivalents are very safe assets that can be are readily converted into cash. Accounts receivable consists of the short-term obligations owed to the company by its clients. Companies often sell products or services to customers on credit, which then are held in this account until they are paid off by the clients. Lastly, inventory represents the raw materials, work-in-progress goods and the company’s finished goods.

Non-Current Assets

Non-current assets, are those assets that are not turned into cash easily, expected to be turned into cash within a year and/or have a life-span of over a year. They can refer to tangible assets such as machinery, computers, buildings and land. Non-current assets also can be intangible assets, such as goodwill, patents or copyright. While these assets are not physical in nature, they are often the resources that can make or break a company - the value of a brand name, for instance, should not be underestimated.

Depreciation is calculated and deducted from most of these assets, which represents the economic cost of the asset over its useful life.

4. Liabilities

On the other side of the balance sheet are the liabilities. These are the financial obligations a company owes to outside parties. Like assets, they can be both current and long-term. Long-term liabilities are debts and other non-debt financial obligations, which are due after a period of at least one year from the date of the balance sheet. Current liabilities are the company’s liabilities which will come due, or must be paid, within one year.

Похожие работы

... value of books would increase, but your value of cash would decrease by the same value, at the same time. This is double entry bookkeeping. Ledger Accounts A ledger account is an item in either the Profit & Loss account (which we'll discuss shortly) or the balance sheet. A Ledger account is either a: • Asset • Liability • Equity • Income • Expense The example of purchasing a ...

... , ключевой вопрос представляется следующим образом: позволит ли полная долларизация путем устранения валютного риска существенно снизить премию, связанную с риском дефолта, по долгам, выраженным в долларах? Изучая доходность различных типов облигаций, можно лучше понять, как рынки воспринимают суверенный риск, или риск дефолта, в отличие от риска девальвации. Суверенный риск может быть измерен ...

... debts and other liabilities of the company which have not been accrued due, or which are liabilities for not liquidated damages. In Re Capital Annuities Ltd[12], it was held that inability to pay debts occurs where company’s present, contingent and prospective liabilities exceed the present value of its assets. So, under balance sheet test, the company is unable to pay its debts if the value of ...

... to fear - опасаться, страшиться to go bankrupt - обанкротиться MODERN BANKING (СОВРЕМЕННАЯ БАНКОВСКАЯ СИСТЕМА) The goldsmith bankers were an early example of a financial intermediary. A financial intermediary is an institution that specializes in bringing lenders and borrowers together. A commercial bank borrows money from the ...

0 комментариев