Навигация

5. Ownership Equity

Ownership equity is the initial amount of money invested into a business. If, at the end of the fiscal year, a company decides to reinvest its net earnings, these retained earnings will be transferred from the income statement onto the balance sheet into the ownership equity account. This account represents a company's total net worth. In order for the balance sheet, total assets on one side have to equal total liabilities plus ownership equity on the other.

6. Read the Balance Sheet

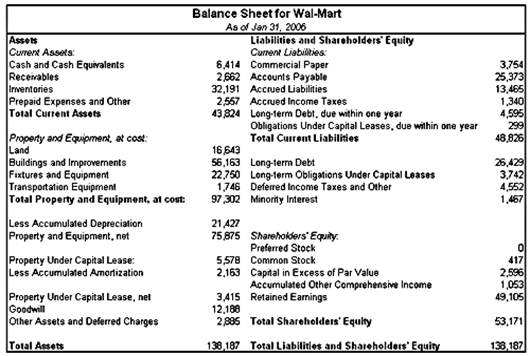

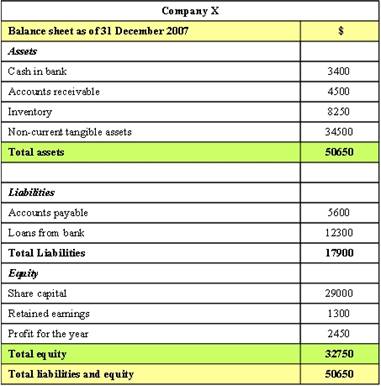

Below is an example of a balance sheet:

As you can see from the balance sheet above, it is broken into two sides. Assets are on the left side and the right side contains the company’s liabilities and shareholders’ equity. It also can be seen that this balance sheet is in balance where the value of the assets equals the combined value of the liabilities and shareholders’ equity.

Another interesting aspect of the balance sheet is how it is organized. The assets and liabilities sections of the balance sheet are organized by how current the account is. So for the asset side, the accounts are classified typically from most liquid to least liquid. For the liabilities side, the accounts are organized from short to long-term borrowings and other obligations.

7. Analyze the Balance Sheet

With a greater understanding of the balance sheet and how it is constructed, we can look now at some techniques used to analyze the information contained within the balance sheet. The main way this is done is through financial ratio analysis.

Financial ratio analysis uses formulas to gain insight into the company and its operations. For the balance sheet, using financial ratios (like the debt-to-equity ratio) can show you a better idea of the company’s financial condition along with its operational efficiency. It is important to note that some ratios will need information from more than one financial statement, such as from the balance sheet and the income statement.

The main types of ratios that use information from the balance sheet are financial strength ratios and activity ratios. Financial strength ratios, such as the working capital, provide information on how well the company can meet its obligations. This can give investors an idea of how financially stable the company is and how the company finances itself. Activity ratios focus mainly on current accounts to show how well the company manages its operating cycle (which include receivables, inventory and payables). These ratios can provide insight into the operational efficiency of the company.

There are a wide range of individual financial ratios that investors use to learn more about a company.

1. Баланс

У фінансовій звітності, баланс або звіт про фінансові ркзультати являє собою баланс персони чи організації. Активи, пасиви та власний капітал вказані за станом на конкретну дату, наприклад, на кінець фінансового року. Баланс часто називають відображенням фінансового стану компанії. З чотирьох основних фінансових звітів, баланс є єдиним документом, що відноситься до конкретного моменту часу.

Баланс компанії складається з трьох частин: активи, пасиви та власний капітал. Основні категорії активів, як правило, перераховуються в першу чергу і слідують за пасивами. Різниця між активами та пасивами відома як власний капітал підприємства; у відповідності з рівнянням бухгалтерського обліку, власний капітал повинен дорівнювати активам за мінусом пасивів..

Інший спосіб відобразити теж рівняння полягає в тому, що активи дорівнюють пасивам плюс власний капітал. Таким чином, баланс представляється, з активами в одному розділі та пасивами і власним капіталом в іншому розділі. Сума цих двох розділів повинна бути рівною, вони повинні бути "збалансовані".

Звіти про цінності кожного облікового запису або рядок в балансі, як правило, підтримуються за допомогою системи обліку відомою як подвійна система бухгалтерського обліку.

Фірма, що має справу виключно з готівкою, може виміряти свої прибутки, вивівши весь залишок на банківському рахунку на кінець звітного періоду, плюс будь-яка готівка на руках. Однак, справжне торгове підприємство не виплачуються відразу, воно нарощує запаси товарів та закуповує будівлі та обладнання. Іншими словами: підприємства мають активи і тому вони не можуть, навіть якщо вони хочуть, відразу ж перетворити їх на готівку в кінці кожного періоду. Справжнє підприємство заборговує гроші постачальникам та податковим органам влади, і власники не відображають свої дійсних прибутків та власного капіталу в кінці кожного періоду. Іншими словами підприємства також мають зобов'язання.

Баланс, також відомий як "заяву про фінансовий стан підприємства", показує активи підприємства, пасиви і власний капітал. Баланс разом з звітом про прибутки і звітом про рух грошових коштів, становлять основу будь-якої компанії у фінансовій звітності. Якщо ви є акціонером компанії, важливо, щоб ви зрозуміли, структуру балансу, як аналізувати і читати його.

Похожие работы

... value of books would increase, but your value of cash would decrease by the same value, at the same time. This is double entry bookkeeping. Ledger Accounts A ledger account is an item in either the Profit & Loss account (which we'll discuss shortly) or the balance sheet. A Ledger account is either a: • Asset • Liability • Equity • Income • Expense The example of purchasing a ...

... , ключевой вопрос представляется следующим образом: позволит ли полная долларизация путем устранения валютного риска существенно снизить премию, связанную с риском дефолта, по долгам, выраженным в долларах? Изучая доходность различных типов облигаций, можно лучше понять, как рынки воспринимают суверенный риск, или риск дефолта, в отличие от риска девальвации. Суверенный риск может быть измерен ...

... debts and other liabilities of the company which have not been accrued due, or which are liabilities for not liquidated damages. In Re Capital Annuities Ltd[12], it was held that inability to pay debts occurs where company’s present, contingent and prospective liabilities exceed the present value of its assets. So, under balance sheet test, the company is unable to pay its debts if the value of ...

... to fear - опасаться, страшиться to go bankrupt - обанкротиться MODERN BANKING (СОВРЕМЕННАЯ БАНКОВСКАЯ СИСТЕМА) The goldsmith bankers were an early example of a financial intermediary. A financial intermediary is an institution that specializes in bringing lenders and borrowers together. A commercial bank borrows money from the ...

0 комментариев