Навигация

Economics. Demand, supply, and elasticity

16495

знаков

0

таблиц

0

изображений

Федеральное агентство по образованию

Государственное образовательное учреждение высшего профессионального

образования

Тульский государственный университет

Факультет Экономики и права

Реферат по дисциплине «Английский язык»

«Economics. Demand, supply, and elasticity»

Выполнил Чернышова Д.В.

группы 720151

Научный руководитель Камаева Л.С.

Тула, 2007

Contents

Introduction 3

1. Economics 4

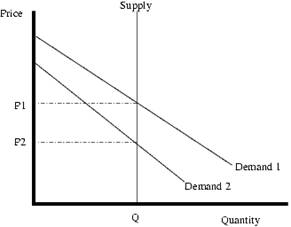

2. Demand, supply, and elasticity 8

Summary 11

List of literature 12

Introduction

Economics is the ancient science. Economics is the method and the instrument of thinking. It is helps us to come to a right conclusion. It always attracts attention of scientific and educated people. Today the interest for economics is growing.

Although for many people concern for the economy goes no further than the price of tuition or the fear of losing a job. Many others, however, know that their job prospects and the prices they pay are somehow related to national trends in prices, unemployment, and economic growth.

The scope of economics is indicated by the facts with which it deals. These consist mainly of data on output, income, employment, expenditure, interest rates, prices and related magnitudes associated with individual activities of production, transportation and trade.

1. Economics

As a scholarly discipline, economics is two centuries old. The first scientist who made extraordinary contributions in economics was Adam Smith. At the age of 28 Adam Smith became Professor of Logic at the University of Glasgow. Some time later he became a tutor to a wealthy Scottish duke. Then he received a grant and with the financial security of this grant, Smith devoted 10 years to writing his work “The Wealth of Nations” which economic science. It was published in 1776. His contribution was to analyze the way that markets organized economic life and produced rapid economic growth. Almost a century later, as capitalist enterprises began to spread, there appeared the massive critique of capitalism: Karl Marx’s “Capital”. Marx proclaimed that capitalism was doomed and would soon be followed by business depressions, revolutionary upheavals and socialism.

In 1936 John Maynard Keynes published “The General Theory of Employment, Interest and Money”. Economics was supposed to help government monetary and fiscal policies to tame the worst ravages of business cycles.

Economics is the study of how society allocates scarce resources and goods. Resources are the inputs that society uses to produce output, called goods. Resources include inputs such as labor, capital, and land. Goods include products such as food clothing, and housing as well as services such as those provided by doctors, repairmen, and police offices. These resources and goods are considered scarce because of society’s tendency to demand more resources and goods than are available.

Most resources are scarce, but some are not — for example, the air we breathe. Its price is zero. It is called a free resource or good. Economics, however, is mainly concerned with scarce resource and goods, as scarcity motivated the study of how society allocates resources and goods.

The term market refers to any arrangement that allow people to trade with each other. The term market system refers to the collection of all markets, also to the relationships among these markets. The study of the market system, which is the subject of economics, is divided into two main theories; they are macroeconomics and microeconomics.

Macroeconomics

The prefix macro means large, indicating that macroeconomics is concerned with the study of the market system on a large scale. Macroeconomics considers the aggregate performance of all markets in the market system and is concerned with the choices made by the large subsectors of the economy — the household sector, which includes all consumers; the business sector, which includes all firms; and the government sector, which includes all government agencies.

Microeconomics

The prefix micro means small, indicating that microeconomics is concerned with the study of the market system on a small scale. Microeconomics considers the individual markets that make up the market system and is concerned with the choices made by small economic units such as individual consumers, individual firms, or individual government agencies.

The distinction between makro- and microeconomics is a matter of convenience. In reality, macroeconomics outcomes depend on micro behaviour, and micro behaviour is affected by macro outcomes.

Economic Policy

An economic policy is a course of action that is intended to influence or control the behavior of the economy. Economic policies are normally implemented and administered by the government. The goals of economic policy consist of value judgements about what economic policy should strive to achieve. While there is some disagreement about the appropriate goals of economic policy, there are three widely accepted goals including:

1. Economic growth: It means that the incomes of all consumers and firms (after accounting for inflation) are increasing over time.

2. Full employment: It means that every member of the labor force who wants to work is able to find work.

3. Price stability: It means to prevent increases in the general price level known as inflation, as well as decreases in the general price level known as deflation.

Economic analysis

Opportunity cost is the important concept in economic analysis. The opportunity cost of a decision or choice that one makes is the value of the highest valued alternative that could have been chosen but was instead forgone. For example, suppose that you is faced with several ways of spending an evening at home. The choice made is to study English (perhaps because there is an English test tomorrow). The opportunity cost of this choice is the value of the highest valued alternative to the time spent studying English. While there may be many alternatives to studying English — making a date, watching TV, talking on the phone — there is only one alternative that has highest value. In this example, the alternative with highest value depends on one’s own preferences. Say, it may be making a date. It would be considered the opportunity cost of studying English. There is also a fundamental assumption used in many economic models ceteris paribus. It is Latin for “all else being equal”.

Common pitfalls in economic analysis

There are two “pitfalls” that should be avoided when conducting economic analysis: the fallacy of composition and the false-cause fallacy. The fallacy of composition is the belief that if one individual or firm benefits from some action, all individuals or all firms will benefit from the same action. While this may in fact be the case, it is not necessarily so. Suppose a hairdresser’s decides to lower the prices it charges on all its services. It believes the lower prices will attract customers away from other hairdressers’. If, however, the other hairdressers’ follow suit and lower their prices by the same amount, then it is not necessarily true that all hairdressers’ will be better off; while more people may choose to cut their hair, each hairdresser’s will receive less money per client, and each hairdresser’s market share is unlikely to change. Hence the profits of all hairdressers’ could fall.

The false-cause fallacy often arises in economic analysis of two correlated actions or events. When one observes that two actions or events seem to be correlated, it is often tempting to conclude that one event has caused the other. But by doing so, one may be committing the false-cause fallacy, which is the simple fact that correlation does not imply causation. For example, suppose that new tape-recorder prices have steadily increased over some period of time and the new tape-recorder sales have also increased over this same period. One might then conclude that an increase in the price of new tape-recorders causes an increase in their sales. This false conclusion is an example of the false-cause fallacy; the positive correlation between the two events does not imply that there is any causation between them. In order to explain why both events are taking place simultaneously, one may have to look at other factors — for example, rising consumer incomes, inflation, or rising producer costs.

Похожие работы

... price of the luxury car decreases, it is actually changing the amount of prestige so the demand is not decreasing since it is a different good. 9. Discrete Example The above discussion of supply and demand can be thought of in terms of individual people interacting at a market. Suppose the following people exist: Alice is willing to pay $10 for a sack of potatoes. Bob is willing to ...

... for the good to amount of needed expenses. Such equality shows us the stability of production and the market which makes the best affectivity of market economy (Matveeva, 2007). Models of market and its impact on productivity Market relationships are influencing on productivity by interrelation of supply and demand. However this influence is not limited only with role of price and pricing. ...

... . For example, in Lover Come Back, Doris Day and Rock Hudson both work in advertising. However, she works while he plays. In What Women Want, Mel Gibson gets all the credit for Helen Hunt's ideas. Advertising and Popular Culture: The Super Bowl Each January advertising moves onto center stage in American popular culture. The occasion is the Super Bowl—itself one of the country's most watched TV ...

s “utility”. Utility and usefulness are different things. For example: a submarine may or may not be useful in time of peace, but it satisfy a want. Many nations want submarine. Economists say that utility is “the relationship between a consumer and a commodity”. Utility varies between different people and different nations. For example: somebody can be a vegetarian and he will be rate the ...

0 комментариев