Навигация

Demand, supply, and elasticity

16495

знаков

0

таблиц

0

изображений

2. Demand, supply, and elasticity

In every market, there are both buyers and sellers. The buyers’ willingness to buy a particular good (at various prices) is referred to as the buyers’ demand for that good. The sellers’ willingness to supply a particular good (at various prices) is referred to as the sellers’ supply of that good.

Reasons for a change in demand

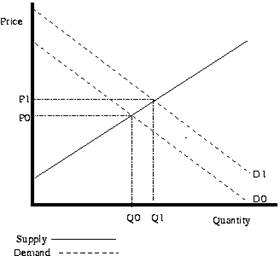

It is important to keep straight the difference between a change in quantity demanded, and a change in demand. There is only one reason for a change in the quantity demanded of some good: a change in its price; however, there are several reasons for a change in demand for the good, including:

1. Changes in the price of related goods: the demand for a good may be changed by increases or decreases in the prices of the other, related goods. These related goods are usually divided into two categories called substitutes (for example, butter and margarine) and complements (for example, shoes and shoelaces).

2. Changes in income: the demand for a good may also be affected by changes in the incomes of buyers. Normally, as incomes rise, the demand for a good will usually increase at all prices, and vice versa. Goods for which changes in demand vary directly with changes in income are called normal goods. There are some goods, however, for which an increase in income leads to a decrease in demand and a decrease in income leads to an increase in demand. Goods for which changes in demand vary inversely with changes in income are called inferior goods. For example, consider meat and bread. As incomes increase, people demand relatively more meat and relatively less bread, implying that meat may be regarded as a normal good, and bread may be considered an inferior good.

3. Changes in preferences: as peoples’ preferences for goods and services change over time, the demand for these goods and services will also shift. For example, as the price for gasoline has risen, automobile buyers have demanded more fuel-efficient, “economy” cars, and fewer gas-guzzling, “luxury” cars.

4. Changes in expectations: if buyers expect that they will have a job for many years to come, they will be more willing to purchase goods such as cars and homes that require payments over a long period of time. If buyers fear losing their jobs, perhaps because of an adverse economic climate, they will demand fewer goods requiring long-term payments.

Supply

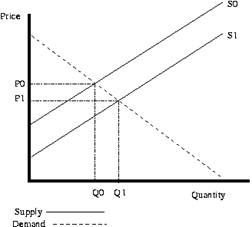

The buyers’ demand for goods is not the only factor determining market prices and quantities. The sellers’ supply of goods and services also plays a role in determining market prices and quantities. According to the law of supply, a direct relationship exists between the price of a good and the quantity supplied of that good. A change in supply is not caused by a change in the price of the good being supplied; that would induce a change in the quantity demanded. A change in supply is caused by other factors, including:

1. Changes in the prices for other goods: suppliers are often able to switch their production processes from one type of good to another. For example, farmers might decide to grow less corn and more wheat on the same land if the price of wheat rises relative to the price of corn.

2. Changes in the prices of inputs: the prices of the raw materials or inputs used to produce a good also cause supply to change. An increase in the prices of a good’s inputs will raise costs to suppliers and cause them to supply less of that good at all prices.

3. Changes in technology: advances in technology often have the effect of lowering the costs of production, allowing suppliers to supply more goods at all prices. For example, the development of pesticides has reduced the amount of damage done to certain crops and therefore has reduced the cost of farming. The result has been an increase in the supply of these crops at all prices.

Equilibrium

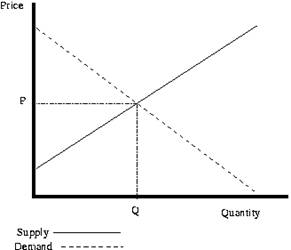

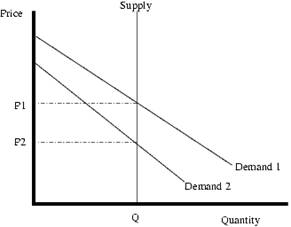

Earlier we have examined the demand decisions of buyers and the supply decisions of sellers, separately. However, in the market for any particular good, the decisions of buyers interact simultaneously with the decisions of sellers. When the demand for a good equals the supply of the good, the market for the good is said to be in equilibrium. Associated with the market equilibrium will be an equilibrium quantity and an equilibrium price.

Elasticity

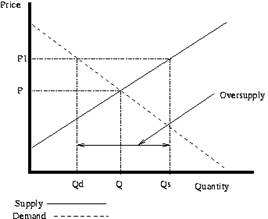

In addition to understanding how equilibrium prices and quantities change as demand and supply change, economists are also interested in understanding how demand and supply change in response to changes in prices and incomes. The responsiveness of demand and supply to changes in prices or incomes is measured by the elasticity of demand or supply.

If the percentage change in quantity demanded is greater than the percentage change in price, demand is said to be price elastic, or very responsive to price changes. If the percentage change in quantity demanded is less than the percentage change in price, demand is said to be price inelastic, or not very responsive to price change. Similarly, supply is price elastic when the percentage change in quantity supplied is greater than the percentage change in price, and supply is price inelastic when the percentage change in quantity supplied is less than the percentage change in price. The price elasticity of demand or supply will differ among goods.

Summary

In this report I consider terms “economics”, “macroeconomics”, “microeconomics”, “economic policy”, “demand”, “supply” and others.

Economics is the study of how society allocates scarce resources and goods. Resources are the inputs that society uses to produce output, called goods. The subject of economics is divided into two main theories; they are macroeconomics and microeconomics. Macroeconomics considers the aggregate performance of all markets in the market system and is concerned with the choices made by the large subsectors of the economy — the household sector, which includes all consumers;

Microeconomics considers the individual markets that make up the market system and is concerned with the choices made by small economic units such as individual consumers, individual firms, or individual government agencies.

An economic policy is a course of action that is intended to influence or control the behavior of the economy. There are goals of economic policy:

1. economic growth;

2. full employment;

3. price stability.

Opportunity cost is the important concept in economic analysis. The opportunity cost of a decision or choice that one makes is the value of the highest valued alternative that could have been chosen but was instead forgone.

In every market, there are buyers and sellers. The buyers’ willingness to buy a particular good (at various prices) is referred to as the buyers’ demand for that good. The sellers’ willingness to supply a particular good (at various prices) is referred to as the sellers’ supply of that good.

It is important to keep straight the difference between a change in quantity demanded, and a change in demand. There is only one reason for a change in the quantity demanded of some good: a change in its price; however, there are several reasons for a change in demand for the good, including:

1. changes in the price of related goods;

2. changes in income;

3. changes in preferences;

4. changes in expectations.

The law of supply: a direct relationship exists between the price of a good and the quantity supplied of that good. A change in supply is caused by factors, including:

1. changes in the prices for other goods;

2. changes in the prices of inputs;

3. changes in technology:

When the demand for a good equals the supply of the good, the market for the good is said to be in equilibrium.

I think studying economics is very important for people. Economics is the study of how society allocates resources and goods. If people know what economics, economic policy, economic analysis are they understand the economic processes.

List of literature

1. Дюканова Н.М. Английский язык для экономистов: Учеб.пособие. – М.: ИНФРА-М, 2006. – 320 с.

2. Большой англо-русский экономический словарь / Составители С.С. Иванов, Д.Ю. Кочетков. – М.: ЗАО Центр-полиграф, 2005. – 620 с.

Похожие работы

... price of the luxury car decreases, it is actually changing the amount of prestige so the demand is not decreasing since it is a different good. 9. Discrete Example The above discussion of supply and demand can be thought of in terms of individual people interacting at a market. Suppose the following people exist: Alice is willing to pay $10 for a sack of potatoes. Bob is willing to ...

... for the good to amount of needed expenses. Such equality shows us the stability of production and the market which makes the best affectivity of market economy (Matveeva, 2007). Models of market and its impact on productivity Market relationships are influencing on productivity by interrelation of supply and demand. However this influence is not limited only with role of price and pricing. ...

... . For example, in Lover Come Back, Doris Day and Rock Hudson both work in advertising. However, she works while he plays. In What Women Want, Mel Gibson gets all the credit for Helen Hunt's ideas. Advertising and Popular Culture: The Super Bowl Each January advertising moves onto center stage in American popular culture. The occasion is the Super Bowl—itself one of the country's most watched TV ...

s “utility”. Utility and usefulness are different things. For example: a submarine may or may not be useful in time of peace, but it satisfy a want. Many nations want submarine. Economists say that utility is “the relationship between a consumer and a commodity”. Utility varies between different people and different nations. For example: somebody can be a vegetarian and he will be rate the ...

0 комментариев