Навигация

Private sector and human-resource development in Georgia

320183

знака

85

таблиц

21

изображение

TBILISI, GEORGIA

Private Sector and Human-resource Development in Georgia

Author: Lasha Martashvili

E-mail: lmg@bk.ru

(18.02.2004)

TABLE OF CONTENTS

1. Government Policies. 5

1.1 Government promotion policies of small and medium size enterprises. 5

1.2 National Investment Agency of Georgia.. 5

1.3 Georgian Investment Center. 5

1.2.1 Government’s Export Promotion Policy. 6

1.2.2 Georgian Export Promotion Agency (GEPA) 9

1.4 Foreign Investment Promotion.. 14

1.3.1 Government’s Foreign Investment Promotion Policy. 14

1.3.2 Foreign Investment Advisory Council (FIAC) 21

1.5 Tax Regime. 23

1.3.3 Taxation System and Tax Rates in Georgia. 23

1.3.4 Existing Taxation Practices. 34

1.3.5 Tax Reform Areas. 38

1.6 Legislative Basis for the Operation of the Private Companies. 44

1.5.1 Law of Georgia on Entrepreneurs (LoE) (Corporate Law) 44

1.5.2 Law of Georgia on Securities Market (SML) 51

1.5.3 Employment Regulations in Georgia. 57

1.5.4 Regulations about Real Estate in Georgia. 59

1.7 The Business Environment in Georgia.. 61

1.8 Institutional Arrangements. 64

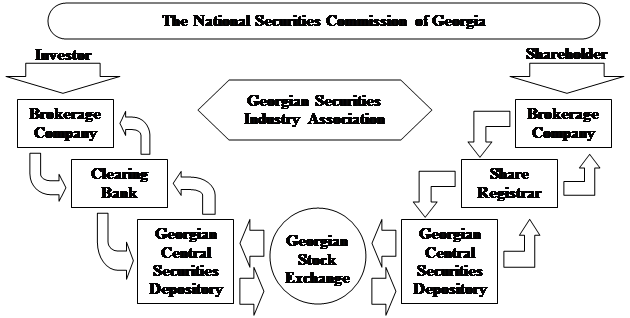

1.3.1 Securities Industry. 64

2. Society.. 65

2.1 Poverty issues. 65

3. Economics. 70

3.1 Main economic indicators. 70

3.2 Agriculture. 77

3.3 Trade. 104

3.4 Construction.. 106

4. Business. 110

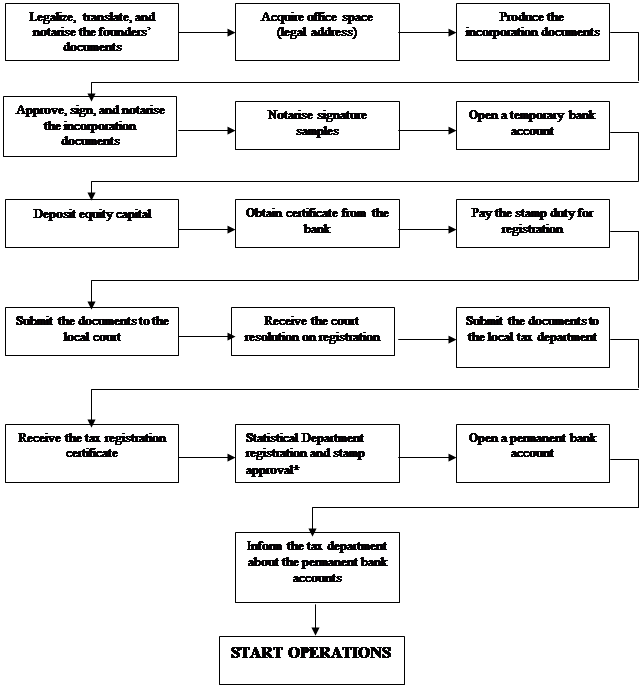

4.1 Company Registration and Licensing System.. 110

4.1.1 Company Registration System.. 110

4.1.2 Company Licensing System.. 117

4.2 Local Enterprises. 119

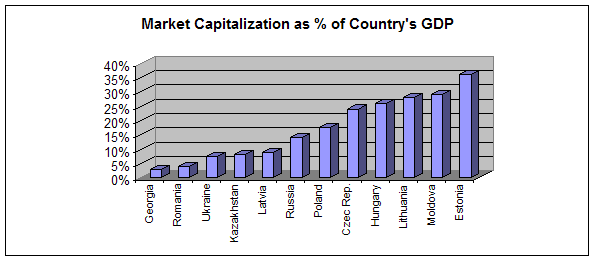

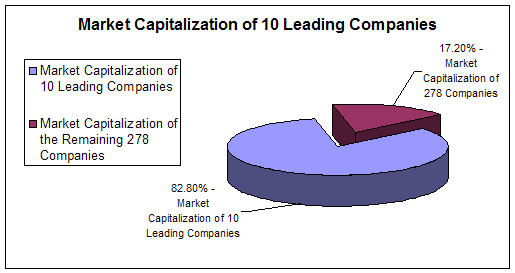

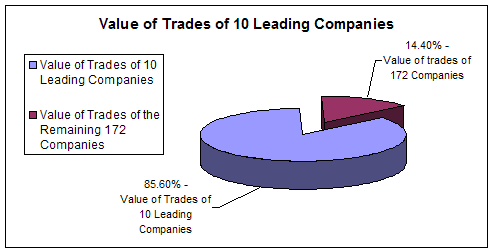

4.1.3 Joint Stock Companies traded at Georgian Stock Exchange. 120

4.1.4 Joint Stock Companies not traded at Georgian Stock Exchange. 132

4.3 Human-Resource Development in the Private Sector. 134

5. Other Donors’ Activities. 138

5.1 The World Bank and IMF. 138

5.1.1 List of the Active World Bank Projects in Georgia. 138

S – Satisfactory. 138

U - Unsatisfactory. 138

5.1.2 List of the Closed World Bank Projects in Georgia. 139

5.1.3 Description of the Closed World Bank Projects in Georgia. 140

5.1.4 The World Bank and IMF Cooperation in Georgia. 149

5.1.5 The World Bank Country Assistance Strategy for Georgia. 154

5.1.6 The World Bank Partners in Georgia. 161

5.2 USAID.. 162

5.3 EBRD.. 162

5.4 EU.. 162

5.5 GTZ.. 163

5.6 CIDA.. 163

5.7 DFID.. 163

5.8 The Government of the Netherlands. 163

5.9 IFAD.. 164

5.10 UNDP. 164

5.11 UNICEF. 164

Currency

(Exchange rate as of 01 Feb. 2004)

| Currency Unit = Georgian Lari (GEL) |

| 1 USD = 2.11 GEL 1.0 GEL = 0.47 USD |

| Abbreviations and Acronyms |

| CAS | Country Assistance Strategy of the World Bank |

| CFAA | Country Financial Accountability Assessment |

| CIS | Commonwealth of Independent States |

| CPIA | Country Policy and Institutional Assessment |

| DFID | Department for International Development, U.K. |

| EBRD | European Bank for Reconstruction & Development |

| EDPRP | Economic Dev’t & Poverty Reduction Program |

| EU | European Union |

| FAO | Food and Agriculture Organization |

| FDI | Foreign Direct Investment |

| FIAS | Foreign Investment Advisory Service |

| FSAP | Financial Sector Assessment Program |

| FSU | Former Soviet Union |

| FY | Fiscal Year |

| GDP | Gross Domestic Product |

| GEL | Georgian Lari |

| GNP | Gross National Product |

| GoG | Government of Georgia |

| GSE | Georgian Stock Exchange |

| GTZ | German Technical Cooperation |

| IDA | International Development Association |

| IDF | Institutional Development Fund |

| IDP | Internally Displaced Persons |

| IFC | International Finance Corporation |

| IMF | International Monetary Fund |

| IOSCO | The International Organization of Securities Commissions |

| JSC | Joint Stock Company |

| KfW | German Financial Cooperation |

|

| |

|

| |

|

| |

|

|

| LLC | Limited Liability Company |

| MDGs | Millennium Development Goals |

| MoF | Ministry of Finance |

| NBG | National Bank of Georgia |

| NGO | Non-Governmental Organization |

| NBG | National Bank of Georgia |

| NGO | Non-Governmental Organization |

| OECD | Organization For Economic Coop’n & Development |

| PER | Public Expenditure Review |

| PPP | Purchasing Power Parity |

| PRGF | Poverty Reduction and Growth Facility |

| PRSP | Poverty Reduction Strategy Paper |

| SAC | Structural Adjustment Credit |

| SATAC | Structural Adjustment Technical Assistance Credit |

| SEC | Security and Exchange Commission |

| SIDA | Swedish International Development Agency |

| SIF | Social Investment Fund |

| SME | Small and Medium Enterprises |

| SRS | Structural Reform Support Project |

| TACIS | Technical Assistance to the CIS (EU) |

| UNDP | United Nations Development Program |

| UNHCR | United Nations High Commissioner for Refugees |

| USAID | United States Agency for International Development |

| VAT | Value Added Tax |

| WTO | World Trade Organization |

|

| |

|

| |

|

| |

|

| |

|

|

1. Government Policies 1.1 Government promotion policies of small and medium size enterprises

[To be described:] "Small and Medium Enterprise State Support Program for 2002 - 2004 in Georgia"

[To be described:] Law of Georgia "On Promotion of Small and Medium Enterprises"

1.2 National Investment Agency of Georgia[To be described:] Law of Georgia "On National Investment Agency of Georgia"

[To be described:] Activities of the National Investment Agency of Georgia

1.3 Georgian Investment Center[To be described:] Activities of the Georgian Investment Centre

1.2.1 Government’s Export Promotion Policy

Foreign Trade Regimes. Reforms carried out in recent years in Georgia, including serious legal reforms, are working successfully to create a favourable foreign trade regime in the country. Since 1995 the following major reforms have taken place in Georgian legislation:

The system of quotas has been eliminated. Products included in the nation's export embargo policy include only works of art and antiques and items of national historical importance. There is no customs duty for exports in Georgia. A fiscal policy aimed at stimulating exports has been introduced whereby all export goods are free of VAT and excise duty;Export of goods requiring an export license have been reduced to the following classes:

Collections and collectors' pieces of zoological, botanical, mineral, anatomical, historical, archaeological, paleonthological, ethnographic or numismatic interest (HS - 9705);

Wood and timber (4401, 4403, 4404, 4406, 4407);

Seeds of Caucasus Pine (120999100);

Ferrous and non-ferrous metal scrap (7204, 7404, 7602).

The system of compulsory registration of foreign trade contracts was eliminated in November 1997.

The establishment of favourable trade regimes with partner countries through bilateral and multilateral agreements has commenced. During the period 1992 - 1998, Georgia signed trade agreements with 22 countries. Agreements on free trade have been signed with eight CIS countries and Georgia already has working free trade agreements with Russia, Ukraine, Azerbaijan, Armenia, Kazakhstan and Turkmenistan. Currently a multilateral agreement on CIS free trade zone is being enforced. According to these agreements signatories to the agreement need not use customs duties and taxes for exports or imports of the goods originated in the territory of one party and destined to the territory of the other party.

Furthermore, Georgia has become a part of several international conventions.

On October 6, 1999 Georgia became a member of the World Trade Organization (WTO) which granted Georgia the status of the Most Favoured Nation with 135 WTO member countries. Through the mechanisms of this organisation, Georgia will be protected from discrimination, unfair competition, falsification and unjustified limitations.

In 1996 Georgia signed an agreement on partnership and cooperation with the European Union which deals with economic relations in almost every sector. In fact the agreement covers all sectors of the economy.

In 1999 Georgia became a member of the Council of Europe with full rights, which will further facilitate trade-economic relations between Georgia and member countries of the European Union.

Many countries have granted to Georgia reductions in import customs taxes to their countries, under the General System of Preferences. These include the countries of the European Union, Switzerland, the Czech Republic, Slovakia, Canada and Japan. This is one of the most important influences on the successful growth of exports for Georgia. The effective use of facilities such as GSP will substantially promote Georgian export development.

Law of Georgia "On Technical Barriers to Trade". The law "On Technical Barriers to Trade" lays down the basis for eliminating the technical barriers to trade during the process of the preparation, adoption and application of the technical regulations, standards and the procedures for the assessment of conformity.

The national technical regulations and standards should not create unnecessary obstacles to trade, which will put national products in favourable conditions. Therefore, the development of the national technical regulations and standards should be carried out on the basis of a direct use of the international standards.

Georgian legislation did not envisage the concept of technical regulations. The concept of technical regulations was defined by Law of Georgia "On Standardization" adopted in 1999. The technical regulations is a legal act, which defines the technical specifications for products or service, which is done directly or by means of referring to Georgian standards and requiring that complying with these standards is compulsory.

The principles of the state standards that are effective in Georgia envisage the application of the national standards on a compulsory basis from the moments of its effectiveness. However, based on the principles that define the standards as voluntary, the international practice envisages two-stage approach to making a standard as mandatory requirement: the standard that was adopted by national body is optional and it may be used by any party, however it will become mandatory, if it is defined by:

The legislation;

Such stipulation is indicated in the technical regulations;

A producer or supplier of services assumed such responsibility by the assessment of conformity.

The first chapter of the present draft law lays down the legal basis for eliminating the technical barriers to trade during the process of the preparation, adoption and application of the technical regulations, standards and the procedures for the assessment of conformity.

It defines the terms, including "Technical barriers to trade", which in fact is the discrepancy in requirements from those used at a national level or in international practice with respect to the technical regulations, standards and the procedures for the assessment of conformity.

It defines the different categories of technical regulations, which include:

Legislative acts, the decrees of the President of Georgia, which consist of the product requirements;

The national standards, the application of which is mandatory;

The agency specific normative acts issued by government bodies, the competency of which, according to the legislation of Georgia, includes laying down the mandatory product requirements.

The second chapter defines the requirements to the content of technical regulations, preparation of technical regulations and procedures for the assessment of conformity, coordination of the activities related to the development of technical regulations, and recognizing the technical regulations of foreign countries as an equivalent to the national technical regulations.

Chapter three defines the procedure of applying technical regulations and standards, which includes making references to standards in technical regulations, fulfillment of standards as a mandatory requirement, fulfillment of standards as a voluntary requirement, and the national arrangements for applying the technical regulations and standards with respect to the national and imported products.

Chapter four defines the principles of providing information relating to technical barriers to trade. The main emphasis is placed on the Central Information Center of Standards, the main function of which is the relationship with the World Trade Organization. The Central Information Center of Standards provides information about the technical regulations, standards and the procedures for the assessment of conformity that are already developed or are in the process of development. It should carry out the coordination of activities of the centers set up in this field by other government bodies.

Chapter five defines the authority and responsibility of the National Standardizing Body and other government bodies.

Chapter six lays down the principles of the state control and supervision on complying with the requirements of technical regulations, as well as the responsibility for violating the requirements of the law.

Chapter seven states that the process of developing technical regulations has to be financed by the state on a mandatory basis.

Chapter eight contains the provisional clauses, which states that the government bodies should adopt and publish those technical regulations, which envisage complying on a mandatory basis with the standards that ensure the quality of products, processes and service, security, protection of human life, protection of the health, property and environment. With this respect it will be significant to employ, whenever developing the technical regulations, the directives issued by the countries that are members of the European Union.

Chapter nine defines the amendments that have to be made into Georgian legislation after this law becomes effective.

The Law of Georgia "On Technical Barriers to Trade" should initiate the practical efforts towards the preparation, adoption and application of the technical regulations, which will be step forward towards setting up voluntary standardization system that is one of the attributes of modern market relationships.

1.2.2 Georgian Export Promotion Agency (GEPA)

The Georgian Export Promotion Agency was set up by the Georgian Government and the European Union's Technical Assistance Programme TACIS with the principal aim of assisting Georgian companies to increase exports and thus to stimulate an improvement in the country's trade balance. The GEPA was established in April 1999. Since then, the German Government's Technical Assistance Programme GTZ (Deutsche Gesellschaft fur Technische Zusammenarbeit GmbH) has also invested in the agency both in its personnel and in its activities.

GEPA supports Georgian business interests in the global marketplace, assists in forging business alliances, facilitates establishment of international business relationships. GEPA provides comprehensive information on business opportunities both for Georgian and overseas companies.

Export Information Center. GEPA Export Information Centre (EIC) promotes Georgian companies and their products on the global marketplace. It offers the services of two Georgian business information officers and a librarian who work in cooperation with specialists from EU countries. The EIC holds a wide range trade information resources including reference materials, manuals and textbooks on exporting, sector related journals from overseas, CD-ROM and online databases, information on local and foreign markets, trade regulations and has wide access to trade leads databases.

The EIC services include but are not limited to:

Providing market information to Georgian exporters

Introducing Georgia and Georgian products to companies around the world

Assisting foreign companies in sourcing products in Georgia

Offering online trade leads both for Georgian exporters and overseas importers

Assisting Georgian companies in developing an export marketing strategy

Overseas Exhibitions and Trade Missions. GEPA is actively involved in preparing overseas business visits for Georgian business groups to meet with new trading partners; we also prepare and part finance Georgian sectors' participation at international exhibitions. Many foreign delegations, commercial and governmental, pay a visit to our agency during their visits to Tbilisi. Study tours for sectors with potential have been organized to Canada, UK and Germany.

With financial assistance from the German government's technical assistance programme, GTZ, GEPA part-finance participation of Georgian exporters in overseas trade shows/exhibitions. GEPA/GTZ have already assisted companies to take part in exhibitions in Germany, France, Italy and the Middle East.

Conditions for participation are that export products must be of export quality, prices examined by German specialists and a group of a minimum of three producers from one sector participates in each exhibition.

Training Center. GEPA offers a wide range of export training courses to Georgian businessmen, civil servants, and commercial banks, on subjects ranging from export pricing to utilizing e-commerce in exporting. All courses are taught by international and Georgian specialists in their given fields of specialization.

A new Training Programme that Georgian Export Promotion Agency offers to Georgian companies differs considerably from the Programme already conducted by GEPA within the framework of previous TACIS project. It includes an In-Company Training that is designed to meet the training needs of companies participating in GEPA's Export Development Program.

Customized programs have been developed for specific companies to increase the professional skills of company managers and staff and thereby help them improve their export activities. In-company training is considered as part of the consultancy service provided by GEPA to existing exporters and to companies with the potential to export. Format and content of training depends on business features of individual companies. Mostly practical exercises and case studies have been used to achieve the best results.

Alongside in-company training, GEPA continues to offer general training in Export Marketing, Export Promotion, Strategic Business Planning etc.

GEPA hopes that new arrangements run in the field of training, will be of real assistance to Georgian companies in enhancing their export marketing activities and in achieving increased export orders.

Publications. GEPA staff prepares a variety of publications for both Georgian exporters and overseas companies. These publications include Export Newsletter, Market Briefs, Fact Sheets and the Directory of Georgian Exporters. Recently a brochure on Georgian viticulture and winemaking was prepared in corporation with the Institute of Viticulture.

Export Newsletter. Export Newsletter is available both in print and electronic formats on our website. It is circulated to Georgian companies and international organizations. It includes information on opportunities outside Georgia for exporters, case studies on successful Georgian and foreign companies and an update on any changes in Georgian, and foreign legislation, which may affect exporters. It also advises of forthcoming exhibitions and incoming buying missions from overseas.

Market Briefs. Market Briefs are prepared in Georgian and are available for Georgian companies interested in specific industries and markets. Market briefs prepared to date are as follows:

1. UK Wine Market

2. Pipes' Market in Italy

3. Organic Food market in Germany

4. UK Nuts Market

5. Timber Market in Germany

6. UK Tea market

7. Intellectual Property - overview

8. EU Fertilizer Market

9. USA and EU Markets for Essential Oils

10. Wine Market in Japan

11. Mineral Waters in Japan

Sample Market Brief: Wine Market in Japan

| ||||||||||||||||||||||||||||||||||||||

Sample Market Briefs: Mineral Waters in Japan

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

1.4 Foreign Investment Promotion 1.3.1 Government’s Foreign Investment Promotion Policy

Removing Administrative Barriers to Investment in Georgia. FIAS (Foreign Investment Advisory Service, a joint service of the International Finance Corporation (IFC) and the World Bank) conducted a study of administrative barriers to investment in Georgia. The principal counterpart for this project was the Presidential Commission on Support of the Private Businesses in Georgia. The Presidential Commission on Support of Private Businesses is the lead counterpart for this project (for more details refer to Paragraph 1.3.1 describing the activities of Foreign Investment Advisory Council - FIAC). The main objective of this study was to identify the major administrative impediments to investment and to recommend the steps for streamlining, simplifying and increasing transparency in order to help improve the environment for business in Georgia. Although the primary focus of the study was foreign investment, the administrative procedures and regulatory framework affect domestic investors as well. Therefore, applying the principle of national treatment (i.e. no preferential treatment for foreign investors), this study is intended to help strengthen the business environment for all investors—domestic and foreign alike.

The study covers the core administrative processes for:

· Establishing a business - including investor entry (visa and residency requirements for expatriates) and business registration.

· Locating a business - including land acquisition, site development, construction and operation.

· Operating a business - including taxation, trade regime and customs, licensing, permits, inspections, intellectual property issues, and product standardization.

Establishing a Business—Investor Entry and Business Registration. The procedures for obtaining entry visas are relatively transparent and present no significant administrative impediments. Most notably, foreign investors and expatriate employees do not require special work or residence permits to live and work in Georgia.

The court registration procedures have been simplified in the past 2 years. However, because of the lack of technical and human capacity, court registrars are unable to fulfill the provisions of the Law on Entrepreneurs aimed at guaranteeing timely service, ensuring public availability of information on companies, publishing data on newly registered companies, and protecting company names. The most pressing issues relate to length of time required to register (2 to 3 weeks) and to retrieve information on companies.

The principal recommendations for improving the business registration process and the access to company records include:

· Modernization of the registration and data filing systems by taking advantage of new technologies (including the internet) to speed up processing and to improve the access to information, as provided under the law.

· Centralization of the court registration system.

· Publication and dissemination of information on business registration procedures, requirements and fees.

· Resolution of the legal provisions for information disclosure under the Law on Entrepreneurs and the Tax Code.

Locating a Business. Locating, acquiring and constructing or rehabilitating real estate for business activities are not perceived as significant problems by either foreign or domestic investors in Georgia. The current system may not pose an overwhelming difficulty for investors because of the low volume of transactions and the institutionalized system of unofficial payments and influence peddling to facilitate the process. However, there are a number of specific areas where regulations, requirements, and procedures need to be clarified, simplified and streamlined. The report includes a number of detailed short and long-term recommendations for strengthening the laws related to the privatization of agricultural land and improving the quality of service provided by the various bureaus responsible for processing the permits necessary for property development and construction in Georgia.

One of the principal recommendations relates to the Law On Privatization of Agricultural Land. The set of laws on privatization of real estate exclude a legal basis for privatization of large agricultural holdings, all of which are presently held under government leases. To the extent that investment in commercial scale agriculture is viewed as having significant potential in Georgia, privatization of larger agricultural holdings is an appropriate next step. A law on privatization of large agricultural holdings is being developed and is an element of the government’s longer-term plan for further development of property relationships.[1] Enactment of this law should be a priority.

Operating a Business - Tax Administration. On the basis of interviews with representatives of the private sector, government officials, and technical assistance experts, it appears that the tax administration system is fraught with problems that seriously constrain the activities of private enterprises. The recurring themes voiced by the private sector as being burdensome for business included the complexity of the tax system, the lack of clarity in some aspects of the Tax Code and the sheer number of taxes itself. Foreign-owned enterprises seem to be particularly affected under the existing system. In keeping with the scope of this study, the discussion is focused on taxation administration. Recommendations on tax policy are confined to those issues that directly affect administrative procedures and impede business activity. It should be noted that the International Monetary Fund, the World Bank and USAID are currently providing assistance to the Government of Georgia on taxation policy issues.

The main recommendations include the following (for more detailed discussion of tax issues please refer to the next paragraph - "1.4 Tax Regime"):

· Adopt and implement the proposed amendments to the Tax Code. These proposed amendments cover a number of policy and tax administration issues. They are broadly in line with IMF recommendations, except the Government proposal for the fixed tax and the elimination of the payroll tax.

· Simplify the procedures for filing VAT. The proposed measures include allowing quarterly, rather than monthly filings for small businesses.

· Establish an effective tax-refund system. The International Monetary Fund has outlined a refund strategy that includes limiting entitlement to immediate refunds, distinguishing claimants with a history of compliance, and using pre-refund audits for high-risk refund claims and post-refund audits for claims of lesser risk.

· Review the micro level target-based system for tax collection. It is important to distinguish between the fiscal macro targets which are an important aspect of revenue administration and micro or firm-level targets which are often arbitrarily established within tax jurisdictions. These targets must be realistic and they should be part of a number of efficiency and effectiveness indicators.

· Improve information compilation and dissemination. Taxpayers must be informed of changes in the Tax Code and related regulations, legal interpretations, and instructions in a timely manner. Also, a credible resource must be established to respond to queries offer binding interpretations of the Tax Code.

Operating a Business – Customs. The State Customs Department (SCD) operates an inland clearance system that requires considerable resources and logistical support for effective control of cargo. In practice, the current system is largely ineffective and prone to fraud and corruption. There is no compendium of the legislation on customs available to the customs service employees or the public. In the absence of common information and an official interpretation of the rules and regulations, the discretionary authority of individual customs officers and offices is strong thereby facilitating corruption. There is significant leakage of cargo transported for inland clearance. Some sources estimate that as much as 50 percent of fuel and cigarette imports are diverted.

Management of the SCD has suffered as a result of frequent changes in the management. Efforts to reform the SCD have been impeded by the lack of political will, competing political agendas, and the frequent changes in leadership. Under these circumstances, the inputs of external advisers have been marginalized and the reforms implemented by previous chairmen have been reversed in many instances. The detailed action plan prepared under the ITS contract and endorsed by the government has been stalled with only marginal progress. The customs reform committee established by the President to lead the reform effort has met irregularly.

The principal recommendations for strengthening and improving the customs service include:

· Implementation of the already approved customs reform program. This is a well developed and comprehensive program that can be implemented over time. It encompasses a number of the IMF and FIAS recommendations. One of the immediate tasks would be to assign priorities for implementation.

· In light of the decision not to renew the ITS contract, it is necessary to immediately develop and implement a framework for carrying out efficient pre-shipment inspection services if it is to be continued after December 30, 2001. The SCD clearly lacks the capacity or the expertise to carry out this function independently.

· Review of the existing regulations for the valuation of cargo and implementation of guidelines that are consistent with the provisions of GATT.

· Revision of the declaration processing procedures to eliminate contact between the import (or broker or freight forwarder) and the customs officer.

· Expansion of the ASYCUDA system to all major customs clearance offices.

· Implementation of risk-based criteria for selecting goods and documents to be examined at all locations where imported goods are cleared.

· Implementation of an information publication and dissemination program.

Operating a Business - Licensing and Permits. The existing regime for licenses has benefited from extensive efforts to streamline and simplify the legal framework for licenses. As a result, the current licensing procedures do not appear to present significant barriers to investment and business activity in Georgia, particularly compared with other former Soviet Union countries. However, some of the sectoral licensing laws and regulations do not conform to the provisions of the framework Law on Licensing.

The Law on Local Charges and related normative acts (including municipal regulations) are not entirely clear in defining the purpose and scope of permits. The criteria and conditions for authorizing and terminating permits (similar to licensing conditions) are not clearly specified in the laws and regulations. In effect, the enforcement of the permit system is arbitrary and subject to abuse of the compliance provisions and the assessment of violations. While this permit regime does not generally impede business in Georgia, it does create unequal conditions for newcomers and arbitrary enforcement can cause significant problems for individual companies.

The main recommendations for strengthening the framework for the system of licensing and permits and facilitating the streamlining and simplification of the current system in Georgia include:

· Passage and adoption of a strong and clear framework law and implementing regulations on the licensing and permit regimes.

· Review and rationalization of the number and level of legally permissible permits to avoid the proliferation of permits for revenue generation.

· Development of a basic set of guidelines on the procedures for processing and enforcing permits (similar to those in place for licenses).

· Development of a monitoring mechanism within the Ministry of Justice that will ensure consistent enforcement of provisions for permits.

· Publication and dissemination of information on the legally sanctioned licenses and permits (e.g., regulations, procedures, documentation requirements, fees and appeals mechanisms).

Operating a Business - Inspections. The passage of the Law on Supervising Entrepreneurial Activity represented the most recent of a series of attempts to streamline the business inspection process by state and local governments. It is, however, too early to assess the effect of this new law. At the time of the FIAS mission, the implementing regulations had not been completed and the law had not been fully implemented.

The main recommendations to strengthen the implementation of the new regime for inspections include:

· Articulate and publish the mandate of each inspectorate as well as information on definitions of violations, criteria for selecting businesses for inspection, the penalties that may be assessed under specific conditions, and the rights and responsibilities of inspectors and businesses.

· Halt extralegal inspectorate activity pending the registration of all sanctioned inspection activities.

· Establish and enforce procedures for conducting on-site inspections.

· Regulate the payment of penalties and fines resulting from inspections to a central cashier in order to avoid on-site payments and minimize opportunities for corruption.

· Coordinate and rationalize the activities of inspection agencies; implement initiatives for joint training and information sharing among inspection agencies; introduce a code of conduct for inspectors; and train inspectors to understand that their primary function is to ensure public health and safety.

Conclusions and Next Steps. There is a general agreement within Georgia that the existing environment for investment needs to improve if the country wishes to attract new FDI flows and secure the expansion of existing investments. This report has focused on the principal administrative barriers that increase the cost and risk of doing business in Georgia.

Pervasive corruption and the apparent lack of political will to implement reforms have emerged as two fundamental issues affecting the business environment in Georgia. While the degree of corruption may not be the worst in the region, it has a negative effect on business activity and increases the risks and costs of doing business in Georgia. The process of streamlining and simplifying administrative procedures must go hand-in-hand with anti-corruption programs. In a similar vein, it should be noted that number of reforms (e.g. Customs reform) have been stalled as a result of resistance to change and the apparent lack of political will effect change.

In addition to making recommendations for solving some of the regulatory, administrative, and institutional issues that need to be addressed in order to improve the business environment in Georgia, the report points out the areas where further review is necessary and where significant technical assistance is already being channeled, albeit with limited impact.

The experience of other countries clearly demonstrates that sustainable change cannot be achieved without government commitment at the highest political levels. Successful and sustained change requires leadership, strong champions, and shared goals among all stakeholders within the government and the private sector. On the basis of shared goals, the process of rationalizing, streamlining, and simplifying bureaucratic procedures can develop, gain momentum, and improve the values of government agencies and transform them into service-oriented organizations. A comprehensive approach to change is necessary, and commitment and time are essential ingredients. Procedural and institutional reforms will require the support of public servants at all levels of government, plus their support for changes in the systems of performance monitoring, evaluation, and rewards.

The Presidential Commission on Support of Private Business already exists as a champion of this initiative. However, the framework for the change agenda must include the participation and inputs of stakeholders at all levels. Stakeholders must be drawn from the public and private sectors. In addition, there is a role for the international donor community in this framework since the incorporation of related donor-sponsored initiatives must be integrated into the change agenda. Chapter V of the report proposes a framework for the development and implementation of the change agenda.

The institutional structure to support the change agenda should include:

· The Presidential Commission. The Commission should serve as the focal point of the change agenda and it should be given the mandate to promote and advocate reforms in collaboration with other parts of the Government.

· An implementation team. The staff of the commission’s secretariat should constitute the core group of the implementation team. The responsibilities of the team would include the development of the Action Plan, coordination of implementation activities, solicitation of donor funds and resources to support reform, coordination of related initiatives, and regular reporting on progress to the Commission.

· A consultative committee. The committee should provide a mechanism for regular consultation with a broad group of stakeholders on various reform initiatives.

The above - mentioned Action Plan should be utilized to document the agreed-upon changes, establish priorities and timeline, provide a basis for accountability, and keep an ongoing record of progress. Therefore, it must be emphasized that the Action Plan is not a static document but one that must evolve over time.

Law of Georgia "On Investment Activity Promotion and Guarantees". On 12 November 1996 the Parliament of Georgia adopted the law of Georgia "On Investment Activity Promotion and Guarantees", which replaced the Law of the Republic of Georgia "On Investment Activity" adopted on 10 August 1991 and the Law of the Republic of Georgia "On Foreign Investments" adopted on 30 June 1995.

The Law defines the legal bases for realizing both foreign and local investments and their protection guarantees on the territory of Georgia. The purpose of the Law is to establish the investment-promotional regime in Georgia.

Investments. Investments shall be deemed to be all types of property and intellectual valuables or rights invested and applied for gaining possible profit in the investment activity carried out in the territory of Georgia, such as:

a) Monetary assets, a share, stocks and other securities;

b) Movable and immovable property (real estate) - land, buildings, structures, equipment and other material valuables;

c) Lease rights to land and the use of natural resources (including concession), patents, licenses, know-how, experience and other intellectual valuables;

d) Other property or intellectual valuables or rights provided for by the law.

Investor. An investor shall be deemed to be a physical (individual) or legal person, as well as an international organization investing in Georgia. A foreign investor shall be deemed to be:

a) A foreign citizen;

b) A stateless person temporarily residing on the territory of Georgia;

c) A Georgian citizen permanently residing abroad;

d) A legal person registered beyond Georgia.

An enterprise with a foreign investment of not less than 25% shall enjoy the same rights as the foreign investor.

1.3.2 Foreign Investment Advisory Council (FIAC)In order to assist foreign investment inflow into Georgia, improve investment climate in the country and support private sector development, it became necessary to create a special government agency, which would serve the above-mentioned goals. Therefore, on March 30, 1997, according to the presidential decree N87, Foreign Investment Advisory Council (FIAC) was created under the supervision of the President of Georgia, intended to assist the development of the private sector and improve the investment environment in the country, to coordinate donors and donor financed projects, to monitor these projects and to ensure a transparency and accounting of foreign aid inflow into Georgia.

The Investment Council operates through its secretariat, which is responsible for the fulfilment of the responsibilities assigned to the Foreign Investment Advisory Council. The Secretariat of the Investment Council works in three directions:

Prepares the Council's meetings;

Cooperates with the donors and coordinates the donor financed projects;

Assists the private sector.

Preparation of the council's meetings. The secretariat of the council plans, prepares meeting and monitors their procession. The meetings are preceded by a preparatory phase, during which the Secretariat identifies priority issues, gathers relevant information, processes, analysis it and identifies a range of possible conclusions. One of the responsibilities of the Secretariat is to control the fulfilment of assigned works and appraise their compliance and produce relevant recommendations.

Cooperation with the donors and coordination of the donor financed projects. Activities related to the cooperation with donors and coordination of the donor-financed projects are a part of the Secretariat's daily job. The Secretariat of FIAC conducts permanent monitoring and control of the projects. Among the donor related activities, a notable obligation of the FIAC Secretariat is to identify the strategy of cooperation with the donors and direct flow of further assistance to relevant channels and to target further projects. Daily work of the FIAC Secretariat includes collection of information on problems related with investment projects and identification of ways of their solution. The council cooperates with short term missions of donors, organizes meetings, drafts agendas and prepares background information for topics of discussion for the Government members as well as for the President of Georgia. The FIAC Secretariat actively works on elaboration of financial-economic, and particularly international relations related legislation of Georgia.

Private sector related activities. To fulfil this obligation the council works in few directions. According to the presidential decree N1324, a Presidential Commission on Support of the Private Businesses in Georgia was formed in the year 2000. By means of close cooperation of the Commission and FIAS, it became possible to study all administrative barriers to investment (see above). As a result, the problems impeding the development of business in Georgia were identified. On the basis of the results of this study, the recommendations were drafted and action plan was compiled, which was approved by the president of Georgia. The commission of cooperation with investors conducts permanent monitoring of fulfilment of the action plan, appraises its fulfilment and prepares relevant recommendations. The Secretariat of Foreign Investment Advisory Council actively cooperates with other donor organizations in terms of the private sector development projects.

1.5 Tax Regime

1.3.3 Taxation System and Tax Rates in Georgia

Legal Framework. The Tax Code of Georgia, adopted on June 13, 1997,[2] is the principal law on taxation policy and administration. Other legislation that regulate taxation include the Administrative Offences Code, the Criminal Code, bankruptcy legislation, customs legislation, the Law on the Road Fund of Georgia, and the Law on the Medical Insurance Fund of Georgia.

The taxation system in Georgia includes both national and local taxes; the latter are set by local authorities following guidelines and limits set forth in the Tax Code. Every taxpayer must register with their regional tax inspectorate and is given a tax identification number, which must be indicated on all tax documents.

Taxes Paid by Individuals, Individual Enterprises.

Income Tax. Income tax must be paid on wages and income earned from economic activity, including income received in non-monetary form. Physical persons, both resident and non-resident, individual enterprises, and entrepreneurs are subject to this tax. Under Georgian law, residents are physical persons in the territory of Georgia for more than 182 days during any 12-month period ending in a given tax year.

An individual enterprise is defined as an entity owned and managed by a single person, an enterprise run solely by family members, or a farm solely owned by an individual or members of that individual’s family. Physical person entrepreneurs are individuals who engage in entrepreneurial activity without first establishing themselves as legal persons (and in accordance with the entrepreneurs law). Physical person entrepreneurs and individual enterprises with annual gross income equal to or less than 24,000 GEL are subject to a presumptive tax in lieu of an income tax. The presumptive tax is described in the next section.

Georgian residents must pay income tax on gross income from all sources (Georgian and non-Georgian) received during the tax year, regardless of where the income was earned or paid, less allowable deductions.

Non-residents must pay income tax, but only on income received from Georgian sources. Non-residents who engage in economic activities through a permanent establishment are subject to profit tax on gross income received during the tax year from Georgian sources connected with the permanent establishment, less allowable deductions.

Taxable income is composed of the following:

· Salaries and wages

· Dividend, interest, and royalty payments

· Income from the lease or rental of property

· Income from the write-off of debts

· Income received from the supply of goods or performance of services

· Gains from the sale of assets

· Income received as a result of the restriction or closing of an entrepreneurial activity

· Income from the sale of shares in an enterprise

· Income in the form of insurance payments paid under agreements for the insurance or reinsurance risk in Georgia.

In addition to monetary wages, benefits are considered wage income and are taxable as part of gross income. Generally, benefits are included in income at the market price at the moment of receipt, reduced by any portion of the benefit paid by the employee. These include: use of an automobile for private service; gifts of goods or gratuitous performance of services; educational assistance to the employee or dependents; and employee expenses reimbursed by the employer.

Table 1.4.1.1 shows income tax rates. Income tax on dividends, interest payments, and payments to non-residents are withheld at the source of payment and are subject to different rates. Dividends and interest payments are taxed at the rate of 10 percent. Dividends and interest payments received by physical persons, taxed at the source of payment, are not subject to additional taxation. Further, taxes paid on the first 3,000 GEL of combined interest and dividends may be applied to reduce the taxpayer’s tax liability, assuming adequate documentation of the tax payment is provided.

Table 1.4.1.1: Income Tax Rates

| Amount of taxable income during the tax year | Tax rate |

| Up to 200 GEL | 12% of the taxable income |

| 201 to 350 GEL | 24 GEL + 15% of the amount in excess of 200 GEL |

| 351 to 600 GEL | 46.5 GEL + 17% of the amount in excess of 350 GEL |

| More than 600 GEL | 89 GEL + 20% of the amount in excess of 600 GEL |

Source: Tax Code.

Tax agents who withhold tax at the source of payment are required to:

· Transfer the tax to the budget when making payments to physical persons;

· When paying wages, issue to the physical person receiving the income (at his or her request) a statement with the person’s name, amount and type of income paid, and amount of tax withheld; and

· Within 30 days of the end of the tax year, present to the tax agencies and, if requested, to the person paid, a statement containing the person’s registration number, total income, and total amount of tax withheld during the year.

Physical person entrepreneurs and individual enterprises are required to submit income tax payments in three instalments, based on their income tax liability for the previous year. Instalments are applied against the taxpayer’s actual liability. Payments may be reduced if income in the current year is expected to be at least 30 percent less than income in the previous year. Taxpayers with no income from the previous year must make payments based on actual income during the previous quarter.

Tax payers[3] are required to submit returns before April 1st of the year following the reporting year. Before the income tax return due date, taxpayers may apply to the tax authorities for an extension of time to submit their returns. Taxpayers who cease entrepreneurial activity must submit a tax return within 30 days of the cessation of activities.

Taxes Paid by Enterprises.

Profit Tax. Profit taxes must be paid by Georgian entities and foreign entities with permanent establishments in Georgia. Foreign entities that do not have permanent establishment presence in Georgia are taxed via a withholding tax at the source of payment, as stated above. Enterprises are defined as:

· Legal persons established according to the legislation of Georgia

· Corporations, companies, firms, and other entities established pursuant to the legislation of foreign states

· Branches and other separate units that are structural units of the entities indicated in the first bullet and that have their own balance sheet and a separate settlement or other account.

Georgian and foreign enterprises are distinguished by place of activity and management. A Georgian enterprise has its place of activity or management within the territory of Georgia, whereas a foreign enterprise has its place of activity or management outside the territory of Georgia. If there is more than one place of management or activity, or the place of management and activity do not coincide, then the predominant location should be used to determine the place of activity or management.

Individual enterprises and physical person entrepreneurs are subject to income tax (or presumptive tax), not profit tax. Branches and other units of an enterprise do not pay profit tax separately, but aggregate profit with the main enterprise, which pays the full profit tax.

Georgian enterprises are taxed on gross income, which includes all income regardless of its source or place of payment, less allowable deductions. The profit tax is a flat rate of 20 percent. Foreign enterprises are also subject to profit tax, the extent to which depends on whether the foreign enterprise is connected to a permanent establishment.

Foreign enterprises that conduct economic activity through a permanent establishment are subject to profit tax on gross income, less deductions, from Georgian sources connected to the permanent establishment. Foreign enterprises that do not conduct economic activities through a permanent establishment must pay profit tax on gross income from Georgian sources (no deductions are allowed), and the tax is withheld at the source of payment. However, non-resident taxpayers (including foreign enterprises) who receive certain types of income (e.g., insurance payments, royalties, management fees, income from works or services) may file a return and claim deductions as if this income was connected to a permanent establishment. The withholding rates for certain types of income are as follows:

· Dividend and interest payments—10 percent

· Insurance proceeds—4 percent

· Telecommunication and transportation services, shipments, and oil and gas transactions—4 percent

· Royalties, management fees, income from performing work or rendering services (except income earned as wages), income from leasing movable property, income from management, financial, and insurance services—10 percent

· Certain oil and gas profits—10 percent.

Foreign enterprises receiving profits from the sale of some stocks, assets, and property not connected to their permanent establishment must pay profit tax, with allowable deductions, on the income from these sales. Annex D provides a listing of profit tax exemptions as well as allowable deductions from gross income.

Table 1.4.1.2 summarizes the asset categories into which fixed assets subject to depreciation are grouped.

Table 1.4.1.2: Summary of Asset Categories

| Group | Types of Fixed Assets | Percentage Depreciation |

| 1 | Passenger automobiles, automobile and tractor equipment for use on roads, special instruments, miscellaneous accessories, computers, peripherals and equipment for data processing and storage. | 20 |

| 2 | Automotive transport, trucks, buses, special automobiles and trailers, machines and equipment for all sectors of industry and the foundry industry, forging and pressing equipment, electronic equipment, construction equipment, agricultural machines and equipment, office furniture. | 15 |

| 3 | Railway, sea, and river transport vehicles; power machines and equipment; turbine equipment; electric motors and diesel generators; electricity transmission and communication facilities; pipelines. | 8 |

| 4 | Buildings and structures | 7 |

| 5 | Assets subject to depreciation not included in other groups. | 10 |

Source: Tax Code.

Buildings and structures are each depreciated separately, whereas the other asset groups are depreciated using the balance of the asset group at the end of the tax year. The balance of the asset group is adjusted for purchases, sales, and repairs. The maximum deduction for repair expenses is 5 percent of the balance of each asset group. Any repairs that exceed 5 percent are added to the balance of the asset group and depreciated as such.

Physical persons who incur a loss in a tax year (i.e., deductions exceed gross income) and who are not connected to employment may not deduct such losses from employment income, but may carry forward and deduct the loss from non-wage income for a period up to 5 years after the tax year in which the net loss occurred. Legal persons who incur a loss in a tax year may carry forward and deduct losses from profit for a period of up to 5 years after the tax year in which the net loss occurred.

Tax credits are subtracted directly from the tax liability. There is a tax credit against Georgian taxes for income and profit taxes paid outside of Georgia, as long as the credit does not exceed the amount of tax charged in Georgia.

A taxpayer may record income and expenses under either the cash basis method or accrual basis method of accounting, but must use the same method for both accounting and tax purposes, and must use the same method throughout the tax year. A physical person must keep records using the accrual basis method for income from entrepreneurial activity.

Profit taxes must be paid in three installments based on the profit tax liability of the previous year. These are:

· Before May 15th: 30 percent of the previous year’s tax liability

· Before August 15th: 30 percent of the previous year’s tax liability

· Before November 15th: 40 percent of the previous year’s tax liability.

Taxpayers who have no taxable income in the previous year make payments according to the actual income of the previous quarter.

Installment payments may be reduced if current year income is expected to be at least 30 percent less than income of the previous year. Permission of the head of the tax agency, requested 1 month before the date of payment is required to do so. Resident legal persons and nonresident legal persons who have income from a Georgian source that is not taxed at the source of payment must submit a tax return before April 1st of the year following the year of the reporting year to the tax agency at the place of registration. Before the due date of a profit tax return, the taxpayer may apply to a tax body for an extension of time to submit the return.

Profit taxpayers who cease their entrepreneurial activity in Georgia must submit an income tax return to the tax agency within 30 days of ceasing activities. Legal persons who decide to liquidate must immediately notify the tax service in writing of their plans to liquidate and must file a profit tax return within 15 days of the decision to liquidate.

Value Added Tax. Value added tax (VAT) is collected at every stage of production and distribution. Persons or enterprises with annual taxable turnover less than 24,000 GEL per year are not required to register with the tax authority and pay VAT, although they may.

An enterprise charges VAT on its sales and pays VAT to the suppliers of materials and providers of services it receives. The enterprise then accounts to the tax department for the difference between the tax that it charged on its sales and the tax that it paid on the goods and services supplied to it. This difference usually results in a net payment to the budget, but in some circumstances it can result in a credit to the enterprise.

An enterprise registered for VAT that carries out a taxable transaction is required to prepare and issue a tax invoice to the person who receives goods or services. VAT invoices are purchased from respective regional tax offices at a cost of 0.18 GEL per invoice. The purchaser is given two copies of the invoice and both the seller and the purchaser must submit one copy to their local tax agencies for control purposes. Buyers and sellers are required to submit VAT declarations every month, no later than the 15th of the month following the reporting period. The total VAT an enterprise pays to the budget each month is the total VAT charged on its outputs (sales) less the total (allowable) VAT paid on its inputs (purchases) during that month. VAT paid on inputs can be credited against VAT paid on outputs if inputs are used for economic activities (offset for charities, entertainment, representative expenses are not allowed) and the enterprise has an invoice of paid VAT. VAT paid on exempt goods or on automobiles cannot be offset. If the input tax exceeds the output tax, the enterprise receives a credit for the excess. VAT on taxable imports is levied and collected by customs agencies.

The VAT rate in Georgia is 20 percent. A zero percent rate applies to exports and the categories of goods and services identified below. Annex D provides a list of VAT exemptions.

Exemption means that producers or suppliers of exempt goods and services do not charge VAT on their output, but cannot claim a credit on the VAT paid on inputs used to produce the exempt output.

Social Taxes. Social taxes include both social and employment taxes and are imposed on monetary and non-monetary wages and other forms of compensation paid to employees, as well as on income earned by physical person entrepreneurs from their economic activities. The social tax rates are summarized in Table 1.4.1.3.

Table 1.4.1.3: Social Tax Rates

| Taxpayers | Taxes Paid by Employers and Entrepreneurs | Taxes Paid by Employees | |

| Social Tax | Employment Tax | Social security Tax | |

| Physical person entrepreneurs and legal persons who pay wages to employees. Physical person entrepreneurs and legal persons who pay physical persons for services. | 27%; not less than 16 GEL per month | 1% | |

| Physical persons who receive remuneration as employees or on a contract basis. | 1% | ||

| Physical person entrepreneurs. | 27%, not less than 16 GEL per month | 1% | |

| Physical persons who carry out non-entrepreneurial economic activities in Georgia. | 27%, not less than 16 GEL per month | 1% | |

Source: Tax Code.

Social taxes must be paid by:

· Physical person entrepreneurs and legal persons who make wage payments to employees working in Georgia or who make payments to physical person who render services in Georgia

· Physical persons receiving remuneration from employment or the performance of services

· Physical person entrepreneurs who conduct entrepreneurial activity in Georgia

· Physical persons who perform non-entrepreneurial activity in Georgia, including lawyers, doctors, notaries, and other professions.

For public organizations of disabled persons as well as enterprises that have a workforce of 70 percent or more disabled persons and pensioners, the 27 percent tax rate is reduced to 10 percent.

Employers who pay wages to employees or to individuals performing services must remit social taxes to the tax administration at the time that wages are paid. Employees’ social taxes are withheld and remitted along with the employer’s social tax payment. Employers are required to submit their social tax returns before the 15th day following the reporting month.

Physical person entrepreneurs and physical persons who carry out economic activities classified as non-entrepreneurial (under the Law on Entrepreneurs) must remit social taxes along with their income taxes. The social tax return must be submitted along with the income tax return.

Excise Taxes. Excise taxes are levied on specific excisable goods produced in Georgia or imported into Georgia. Unless exempted, all physical and legal persons who produce excisable goods on the territory of Georgia or who import excisable goods must pay excise taxes. Exports of excisable goods are taxed at a zero rate.

Several products are exempt from excise taxes, including:

· Alcoholic beverages produced by a physical person for personal consumption

· The import of 2 litres of alcoholic beverages and 200 cigarettes by a physical person for personal consumption

· The transit and temporary import of excisable goods into the customs territory of Georgia

· The re-export of excisable goods

· The import of automobiles and tires for humanitarian aid during a natural disaster

· Aviation fuel to be supplied on board for international flights

· Import or supply of oil products necessary to carry out oil and gas transactions (specified by the oil and gas law of Georgia).

Excise taxes must be paid up to the 10th of the next month after carrying out the taxable transaction. The taxable transaction for products produced in Georgia is considered to occur at the earlier of 90 days from the delivery (transfer) of goods or the moment of payment. In the case of imports, the taxable transaction is considered to occur at the time the goods are imported, and the excise tax is collected by customs agencies. For excisable products subject to excise stamping, the taxable transaction is considered to occur at the time the goods are delivered, and the total amount of excise must be paid upon purchasing the stamps. Excise stamps are required for most imported and domestically produced alcohol products and tobacco products, except for pipe tobacco.

For goods produced on the territory of Georgia, the amount of the taxable transaction is the payment received or to be received by the taxpayer from the customer, excluding the amount of the excise tax and VAT. This amount cannot be less than the wholesale market price excluding the excise tax and VAT. For goods sold at the retail level, the amount of the taxable transaction is the market price of the goods at the wholesale level not including the amount of the excise tax and VAT. For alcohol products, the amount of the taxable transaction is based on the volume of alcoholic beverages. For imported goods, the amount of the taxable transaction is the customs value of the goods determined in accordance with the customs legislation of Georgia (but not less than the wholesale market price, excluding the excise tax and VAT) plus the amount of duties and taxes payable on the import of the goods (except for the excise tax and VAT).

Property Taxes. Georgian enterprises, branch offices, and other similar subsidiary enterprises that have an independent balance sheet and settlement account, foreign enterprises operating through a permanent establishment, and organizations whose property or part of property is used for economic activity must pay property tax.

Property subject to this tax includes fixed assets, installed equipment, uncompleted capital investment, intangible assets that are listed on the balance sheet of an enterprise, as well as such property listed on the balance sheet of an organization and used for economic activity. For foreign enterprises, only property connected with the permanent establishment of the enterprise is subject to property tax.

The property tax rate is 1 percent of the value of the property. The tax is due in four equal payments, before February 15th, May 15th, August 15th, and November 15th.

Tax on the Use of Land. Physical and legal persons who are owners or users of land plots, including land used for agricultural and non-agricultural purposes, are subject to tax on the use of land.

The base rate of the tax for the use of nonagricultural land is 0.24 GEL per square meter of land. This tax is due in equal parts before August 15th and before November 15th of the reporting year.

The base rates for agricultural land are set on a per hectare basis and vary depending on location and use. This tax is due on or before November 1st of the reporting year.

Tax on Economic Activity. This local tax is paid by all physical and legal persons engaged in any economic activity on the territory of a corresponding city (region).

This tax rate is set by local governments, but cannot exceed 1 percent of income (less material expenditures and VAT). For port services (loading and unloading ships) the maximum rate is 2 percent of income (less VAT).

Other Taxes.

Tax on the Transfer of Property. This tax is imposed on the transfer of real estate located in Georgia, inheritances and gifts, and the transfer of motor vehicles. The transferee is subject to the tax. Transfers of title, as well as certain leases of real estate are taxable.

The taxable amount is the amount of compensation transferred (but not less than the market price), including assumed indebtedness. In the case of a lease or tenancy, the taxable amount is determined by discounting the amount payable under the lease or tenancy agreement.

The tax rate on the transfer of real estate is 2 percent of the taxable amount. The tax is due prior to the registration of the documents transferring the property. If the property is not registered, the tax is due at the time the property is transferred.

For property received as inheritance, the tax is due no later than 6 months from the receipt of documents transferring title. For property received as gifts, the tax is due within 1 month of the transfer.

Tax on the Use of Natural Resources. Physical and legal persons engaged in any activity that requires a license for the use of natural resources (with the exception of land) owned by the state must pay this tax. The tax is imposed on the volume of natural resources extracted.

The tax rates vary by natural resource. For minerals, the rate is between 1 and 15 percent (of the price of the mineral resources extracted), timber 2–34 percent, water 3–10 percent, animals 2–55 percent.

The tax for the use of natural resources is due before the 15th of the month following the reporting month. However, the tax for timber and flora resources should be paid at the time of their transportation from the forest; the tax for water resources should be paid before December 1st of the relevant year; and the tax on hunting birds in migration should be paid on receipt of the license.

The tax on natural resources must be paid within 3 months after receiving the license for using the natural resources.

Exempt from this tax are the mineral resources gained in the course of underground construction. In addition, the tax rate is reduced by 70 percent for use of natural resources in connection with scientific and cultural activities and for users of natural resources that have carried out restoration or replacement of natural resources from their own funds, within the limits of the volume of restored resources.

Environmental Taxes. This tax must be paid by physical and legal persons engaged in any activity listed in categories 1–4 of the Law of Georgia on Environmental Permits (October 15, 1996), who pollute the environment from fixed sources or who import or produce gasoline, diesel fuel, kerosene, natural gas (except as used as a raw material for production of goods), or liquid gas.

Tax rates are based on the pollutant emitted, whether it is emitted into the atmosphere or water (either directly or through sewers and storm drains), and geographic region. For other items the tax is based on the amount imported or produced. Imported goods that are later exported are exempt from this tax.

Tax rates apply to pollutants emitted within limits set by environmental laws. Pollutants emitted in excess of established limits are subject to a fine equal to five times the tax rate for pollution within the limit (see the section on fines and penalties below).

Taxpayers who pollute the environment from fixed sources must submit a tax return certified by the Ministry of Environment and Natural Resource Protection to the tax agency and pay the tax by the 15th of the month following the reporting quarter. Taxpayers who produce or supply gasoline, diesel, kerosene, natural gas, or liquid gas must submit a tax return by the 15th day of the month following the reporting month.

Taxpayers who import any products subject to the pollution tax must pay the tax before the customs agency clears the products. Customs may clear the products only after the tax agency issues a receipt indicating that the tax has been paid.

1.3.4 Existing Taxation PracticesBackground. Georgia was one of the first CIS countries to codify its tax legislation in a comprehensive Code. However, since its adoption in 1997, there have been numerous amendments, which have considerably reduced the consistency of the Code. Some of the mayor changes in recent amendments include: i) changes in the tax rates for tobacco products and the tax rates of the motor vehicles ownership tax; ii) repealing provisions in the Code allowing the tax administration to seize and sell delinquent taxpayers’ property; iii) introduction of exemptions from property taxation for enterprises and physical persons in mountainous regions. The IMF carried out a review of tax policy in 2000 and a number of the recommendations from this review were actually included in a tax reform package prepared by the Ministry of Finance in September 2001. However, this package has not been presented to Parliament so far. Key issues remaining on the tax policy side are:

Unstable tax policy framework. The history of tax policy changes in Georgia since adoption of the tax code demonstrates a lack of long-term policy planning and a focus on short-term policy measures, disregarding the general consistency of the Code. Such approach has led to constant changes to Article 273 (on transitional provisions). Even fundamental policy changes are not introduced as permanent features of the tax system, but as temporary ones. A typical example is the cigarette taxation, which has been modified six times (!) since the Code entered into force. New taxation schemes are often introduced late in the year, for short periods of time and without clarification as to their duration. The current taxation scheme for tobacco products was introduced for the year 2001 only on December 2000 and was extended for another year through another amendment to the Code on December 2001. An even worse case is the excise tax on the importation of pyrolysis liquid products which was set at a rate of 400 GEL per ton on December 2000 and reduced to 50 GEL per ton less then four month later. There are numerous similar examples of short-term tax policy measures and frequent changes of tax legislation Such an approach neither allows the business community to calculate its tax burden over a longer period of time, nor does it permit the revenue authorities to design appropriate taxation strategies and develop a long-term planning of resource mobilization. The strong influence of lobbies in Parliament and the obvious tendency of parliamentarians to further narrow the tax base by granting sector and specific exemptions and rate reductions also contributes significantly to the low quality of tax policy making in Georgia.

VAT Threshold. Currently, VAT registration is mandatory for businesses with an annual taxable turnover of 24,000 GEL or more (and voluntary for a businesses below this threshold).[4] As a result of the low registration threshold, the tax administration has to deal with a large number of small businesses as VAT taxpayers who contribute little to total VAT revenues. For example, an increase of the threshold from 24,000 to 100,000 GEL would reduce the number of mandatory taxpayers from around 13,000 to 3,200. It would at the same time reduce the total VAT collection by around 23 percent. A reduction in the number of taxpayers could substantially facilitate the administration of the tax and help combat VAT evasion by permitting a more comprehensive cross-checking of VAT invoices and making it more difficult to establish shell companies for evasion purposes. [5]However, this result can only be achieved if the scope for voluntary registration is reduced. The Ministry of Finance therefore should consider to limit voluntary registration, e.g. by excluding businesses with a turnover below 50,000 GEL.

VAT Distortions. There is increasing frustration with the performance of VAT and the distortions its creates because the tax net is narrow and businesses are often unable to deduct VAT payments on their inputs. First, despite the low threshold, the number of 17, 000 businesses registered is quite low by international standards. Second, a true VAT, which is supposed to avoid tax cascading and economic distortions, requires a prompt and full refund of the part of the tax on inputs which exceeds the tax due on outputs. This is especially important for exporters. In Georgia the amount of unpaid VAT refunds is large (about 29 million GEL at the end of 2001). Tax inspectors should eliminate the practice of treating VAT as advanced payments against future tax liabilities in order to meet their monthly revenue targets (see section on tax administration below). Third, while many countries have introduced limited exemptions or reduced rates in their VAT laws to reduce regressive elements of the tax, the scope of tax privileges in the Georgian VAT continues to increase, and the country has embarked on the dangerous path to use tax privileges as a way to compensate for administrative or legal deficiencies.

Frustration with the distortion effects of the VAT has caused some policy makers to consider whether to replace the VAT with a sales tax. The objective would be to reduce compliance risks by applying the tax to one stage of the business cycle only. There are serious concerns regarding this idea. VAT despite its relatively low efficiency has become the main revenue source, contributing 45 percent to total gross tax revenues in 2001. Experience in other countries shows that sales taxes have a far lower revenue potential than the VAT, because it does not capture the total value added in the production and distribution phases and their rates normally are not higher than 5 percent--because of administrative difficulties. In addition, compliance risks and compliance management challenges would not be reduced because collection would have to rely on the retail sector which is more difficult to administer. Rather than replacing the VAT with a sales tax, the focus should be to improve VAT administration and actually implement the key principles of the tax, such as an effective refund system for exporters. A performance of the tax improves; consideration could then be given later to lowering the standard VAT rate.

Proposed simplified tax. To compensate for the revenue loss caused by increasing the VAT threshold, MoF plans to introduce a simplified tax for taxpayers who are not registered for VAT, and to modify the current presumptive tax for individual enterprises, which raises relatively little revenues (in 2000 actual presumptive tax collection was only 5 million GEL or 0.7 percent of total tax revenues), by changing it to a fixed tax with a broader tax base. The MoF proposal is to levy the simplified tax rate of 7 percent on gross income, which will require some basic accounting. The fixed tax will, similar to the current presumptive tax, be based on the nature of the business activity, the size of the business and the business location; it will include more types of small businesses than the presumptive tax. Although some (Foreign Investor Advisory Service (FIAS) December 2001 report[6]) consider a fixed tax to be extremely complicated, it need not be so. The fixed tax, if well designed, can be transparent and easy to administer tax. It offers no scope for negotiation to taxpayers, does not require detailed bookkeeping, and could reduce the opportunity for corruption and the compliance costs for taxpayers. There are some issues regarding this presumptive taxation scheme:

The combined fixed tax and simplified tax is supposed to compensate for the increase of the VAT threshold. However, estimated revenues from the fixed and the simplified tax are 27 million GEL, which is far less than the expected decrease in VAT revenues. While the increase of the VAT threshold and the introduction of the fixed tax are laudable reforms, the revenue impact of the reform will need to be studied further.