Навигация

THE BASIS FOR THE ACCOUNTING PROCESS

34885

знаков

21

таблица

26

изображений

2. THE BASIS FOR THE ACCOUNTING PROCESS

The basis for the accounting process is the accounting equation. It shows the relationship among the firm's assets, liabilities, and owner's equity.

Assets are the items of value that a firm owns — cash, inventories, land, equipment, buildings, patents, and the like.

Liabilities are the firm's debts and obligations — what it owes to others.

Owner's equity is the difference between a firm's assets and its liabilities — what would be left over for the firm's owners if its assets were used to pay off its liabilities.

The relationship among these three terms is the following:

Owners' equity = assets - liabilities

(The owners' equity is equal to the assets minus the liabilities)

For a sole proprietorship or partnership, the owners' equity is shown as the difference between assets and liabilities. In a partnership, each partner's share of the ownership is reported separately by each owner's name. For a corporation, the owners' equity is usually referred to as stockholders' equity or shareholders'equity. It is shown as the total value of its stock, plus retained earnings that have accumulated to date.

By moving the above three terms algebraically, we obtain the standard form of the accounting equation:

Assets = liabilities + owners' equity

(The assets are equal to the liabilities plus the owners' equity)

3. A BALANCE SHEET

A balance sheet (or statement of financial position), is a summary of a firm's assets, liabilities, and owners' equity accounts at a particular time, showing the various money amounts that enter into the accounting equation. The balance sheet must demonstrate that the accounting equation does indeed balance. That is, it must show that the firm's assets are equal to its liabilities plus its owners' equity. The balance sheet is prepared at least once a year. Most firms also have balance sheets prepared semi-annually, quarterly, or monthly.

4. AN INCOME STATEMENT

An income statement is a summary of a firm's revenues and expenses during a specified accounting period. The income statement is sometimes called the statement of income and expenses. It may be prepared monthly, quarterly, semiannually, or annually. An income statement covering the previous year must be included in a corporation's annual report to its stockholders.

5. THE IMPORTANCE OF THE ABOVE TWO STATEMENTS

The information contained in these two financial statements becomes more important when it is compared with corresponding information for previous years, for competitors, and for the industry in which the firm operates. A number of financial ratios can also be computed from this information. These ratios provide a picture of the firm's profitability, its short-term financial position, its activity in the area of accounts receivables and inventory, and its long-term debt financing. Like the information on the firm's financial statements, the ratios can and should be compared with those of past accounting periods, those of competitors, and those representing the average of the industry as a whole.

|

|

|

|

|

|

|

|

|

|

Exercises

I. Translate into Russian.

Accounting; bookkeeping; accounting information; lender; stock; stockholder; financial statement; balance sheet; income statement; assets; liabilities; owners' equity; bond; debt; annual report; profitability; accounting period; return on investment; soundness of investment; issue of stocks and bonds; revenue; profit; account receivable; transaction; amount; own; owner; relay on; report; borrow; deal with; confirm; approve; provide; compare.

II. Find the English equivalents.

Бухгалтерский учет (бухучет); точная и своевременная информация; акционер;кредитор; ведомство (агентство); отчет

(доклад); балансовый отчет; отчет о доходах; отчетный период; счетоводство (бухгалтерия); финансовая информация; прибыль (доход); выгода (прибыль); прибыль на инвестированный капитал; дебиторская задолженность; обязательство; денежное обязательство (пассив); платежная ведомость; акция (ценная бумага); активы; долг; счет прибылей (иубытков); ежегодный отчет; доходность; собственный акционерный капитал; одобрять; сравнивать; подтверждать; занимать (брать взаймы); обрабатывать (информацию).

III. Fill in the blanks.

1. Managers, lenders, suppliers and government agencies relay on the information contained in two ....

2. These two reports — the balance sheet and ... — are summaries of a firm's activities during a specific time period.

3. The basis for the accounting process is ....

4. Assets are the ... that a firm owns.

5. Liabilities are the firm's debts and ....

6. Owners' equity is the difference between a firm's ... and its liabilities.

7. A balance sheet is ... of a firm's assets, liabilities, and owners' equity accounts at a particular time.

8. A balance sheet must demonstrate that the accounting ... does indeed balance.

9. An income statement is a summary of a firm's revenues and

... during a specific accounting period. >

10. The information in these two financial statements becomes

more important when it is... with corresponding information

for previous years or past... periods.

IV. Translate into English.

1. Бухгалтерский учет — это процесс систематического сбора и сообщения финансовой информации.

2. Балансовый отчет и отчет о доходах являются (are) основой процесса бухучета.

3. Балансовый отчет (или отчет о финансовом положении) — это (is) обобщенный отчет об активах фирмы, пассивах и собственном акционерном капитале.

4. Отчет о доходах — это обобщенный отчет о доходах и расходах за (during) конкретный отчетный период.

5. Основой процесса бухгалтерского учета является буху-четное уравнение.

6. Согласно (according to) бухучетному уравнению активы равны пассивам (денежным обязательствам) плюс собственный акционерный капитал.

7. Собственный акционерный капитал—это разность между активами и пассивами.

8. Балансовый отчет должен показывать, что бухучетное уравнение балансируется.

9. Результаты (results) балансового отчета должны сравниваться (be compared) с результатами за (for) прошлый отчетный период.

10. Эта информация дает картину доходности фирмы, ее финансового положения и ее деятельности в области (area) дебиторской задолженности, товарных запасов и долгового финансирования.

V. Questions and assignments.

1. What is accounting? Give a short definition.

2. Is it possible to manage a business operation without accurate and timely accounting information?

3. Who needs accounting information? Explain why.

4. What is the basis for accounting process?

5. State (изложите) the standard form of the accounting equation.

6. What is a balance sheet? Give a short definition.

7. What must a balance sheet show?

8. What is an income statement?

9. What can be computed from the information contained in a balance sheet and an income statement?

|

|

10. Do the ratios computed from this information provide a picture of a firm's profitability and its financial position?

11. Is this information for competitors?

VI. Read and translate this newspaper advertisement.

|

|

|

|

|

|

VII. Answer the questions.

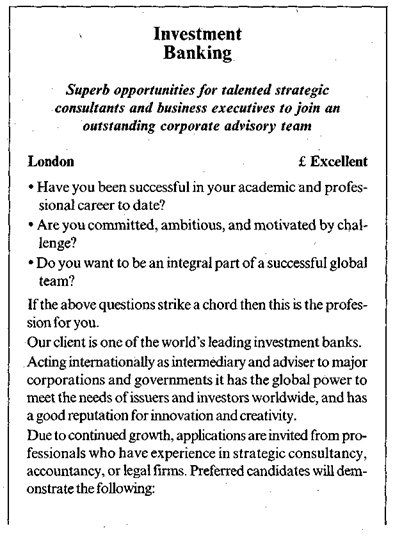

1. What is the name of the firm that has published this ad (advertisement)?

2. Who is the firm's client?

3. What information have you got about the bank for which the firm works?

4. What kind of (каких) specialists does the firm invite?

5. What kind of experience must the invited professionals have?

6. Does experience in accountancy matter (имеет значение)1

7. What will preferred candidates demonstrate?

8. What chief traits (основные черты) of character must the applicants have?

9. Is it necessary to send a full curriculum vitae to Michael Page City firm?

10. What words in the ad characterize the team within which the selected applicants will work?

Unit 8

Operations Management

Operations management consists of all the activities that managers engage in to create products (goods, services, and ideas). Operations are as relevant to service organizations as to manufacturing firms. In fact, production is the conversion of resources into goods or services.

1. A technology is the knowledge and process the firm uses to convert input resources into output goods or services. Conversion processes vary in their major input, the degree to which inputs are changed, and the number of technologies employed in the conversion.

2. Operations management often begins with the research and product development activities. The results of R&D may be entirely new products or extensions and refinements of existing products. The limited life cycle of every product spurs companies to invest continuously in R&D.

3. Operations planning is planning for production. First, design planning is needed to solve problems related to the product line, required production capacity, the technology to be used, the design of production facilities, and human resources. Next, operational planning focuses on the use of production facilities and resources. The steps in this periodic planning are (1) selecting the appropriate planning horizon, (2) estimating market demand, (3) comparing demand and capacity, and (4) adjusting output to demand.

4. The major areas of operations control are purchasing, inventory control, scheduling, and quality control. Purchasing in-

|

|

volves selecting suppliers and planning purchases. Inventory control is the management of stocks of raw materials, work process, and finished goods to minirnize the total inventory cost. Scheduling ensures that materials are at the right place at the right time — for use within the facility or for shipment to customers. Quality control ensures that products meet their design specifications.

5. Automation, the total or near-total use of machines to do work, is rapidly changing the way work is done in factories and offices. A growing number of industries are using programmable machines called robots to perform tasks that are tedious or hazardous to human beings. The flexible manufacturing system combines robotics and computer-aided manufacturing to produce smaller batches of products more efficiently than the traditional assembly line.

|

|

|

|

Похожие работы

... changing his name from Maury, the name of a Bascomb, will somehow avert the disastrous fate that the Compson blood seems to bring. This overwhelming sense of an inescapable family curse will resurface many times throughout the book. Summary of June Second, 1910: This section of the book details the events of the day of Quentin's suicide, from the moment he wakes in the morning until he leaves ...

... озвончения в середине слова после безударного гласного в словах французского происхождения. Зав. кафедрой -------------------------------------------------- Экзаменационный билет по предмету ИСТОРИЯ АНГЛИЙСКОГО ЯЗЫКА И ВВЕДЕНИЕ В СПЕЦФИЛОЛОГИЮ Билет № 12 Дайте лингвистическую характеристику "Младшей Эдды". Проанализируйте общественные условия национальной жизни Англии, ...

... car manufacturing world. On July 24 and July 31 of 1998, the European Commission and the Federal Trade Commission, respectively, approved the merger of Chrysler and Daimler-Benz Corporation, and appearance of Daimler-Chrysler. This merger is classified as a “horizontal merger.” In order to become the largest car-producing corporation in the world, Daimler-Chrysler has to acquire or merger ...

... правильным вариантом поведения компании для достижения эффективного долгосрочного функционирования и успешного развития является уделение повышенного внимание осуществлению анализа внешнего и внутреннего окружения. Это подразумевает проведение комплексного анализа, который может быть проведен с использованием вышеперечисленных методик, который дает достаточно ясное и объективное представление о ...

0 комментариев