Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

Европейская денежная система

Европейская денежная система

355162

знака

0

таблиц

0

изображений

European Monetary System and European Currency

Based on selected papers kindly provided by the European Central Bank

Compiled by Dm. Evstafiev

for the students of the School of Political Science

at St. Petersburg State University

St. Petersburg

1999

Developments in the Financial Sector in Europe

following the Introduction of the Euro

Speech by Dr. Willem F. Duisenberg,

President of the European Central Bank,

to be delivered at the Third European Financial Markets Convention

Milan, 3 June 1999

1. Introduction

The period of the five months following the introduction of the euro has been very rich in new events, with significant developments taking place both in the continental securities markets and in the financial system as a whole. Although experience has been gathered over a relatively short period of time, I am tempted to make two observations of a fundamental nature.

The first observation is that developments following the introduction of the euro do not imply that the euro area is set to become a financial fortress whose financial markets and institutions would be cut off from the rest of the world. In fact, market participants residing outside the euro area seem to be taking a keen interest in the financial markets of the euro area. "Core Europe", so to speak, has become more interesting to outsiders as the breadth and liquidity of its financial markets has increased.

The second observation is that the euro can be expected to have a significant influence on the structure of the financial system by bringing about more securitisation. A traditional feature of the financial system of continental Europe has been a marked dependency on the funds intermediated by banks. This feature contrasts with the financial system of the United States which is much more securitised. For instance, corporate bonds have not been very widely issued in the euro area, and stock market capitalisation - relative to the size of the economy - is much lower in the euro area than in the United States. There are good reasons to believe that a process of securitisation will gather pace in the euro area now that the single currency is in use. This view seems to be shared by many observers and I shall, in the course of my remarks, provide some arguments in its favour.

In my remarks today, I should like to discuss the structural changes in the financial sector, in particular those that have occurred as a result of the launch of new product types and the changing nature of public and private institutions. I shall address developments in the money markets, the bond markets and the equity markets as well as the process of adaptation of banking institutions to their new environment.

2. Money markets

The money markets of the euro area became rapidly integrated after the introduction of the euro despite the fact that their structures had previously been quite different at the national level. Transaction volumes and measures of bid-ask spreads on the various money market instruments both indicate that the markets reached a very high level of liquidity very rapidly in the course of January 1999 and have subsequently retained it.

The high degree of integration of the euro area money markets is, first of all, a result of the single monetary policy, which is conducted through the harmonised operational framework of the Eurosystem. This integration has also been made possible by the significant and increasing integration of payment systems. Cross-border payments processed by TARGET accounted for more than 37% of the value of all real-time payments (domestic and cross-border) effected by credit institutions in March and April 1999. Moreover, the continuously high use which our counterparties make of the correspondent central banking model (or CCBM) for the cross-border transfer of collateral in monetary policy operations is an important indication of area-wide integration. This is evidenced by the fact that cross-border collateral currently represents around 25% of the total amount of collateral in custody in the context of the Eurosystem's monetary policy operations.

Taking a closer look at the various instruments traded in the money markets, a feature that is worthy of note is that market participants in the 11 countries of the euro area have shown an increasing tendency to demonstrate a similar reliance on each instrument type. For example, what we call "overnight indexed swaps", which are swaps indexed on the overnight reference interest rate EONIA, have become an important derivative instrument in the money markets of the euro area. This can be seen from the low level of quoted bid-ask spreads and the high turnover relative to other major international markets. Both indicators show a high level of liquidity in this instrument. Another type of instrument of interest in the money market (but also at the fringe of the bond market) is that of the repurchase agreement. The development of more integrated repo markets in the euro area will obviously accompany the development of area-wide securities trading, settlement and custody systems. This will reduce transaction costs and improve efficiency for the cross-border transfer of securities through repurchase operations.

Looking ahead, other developments in the money markets are expected in the coming months. There are aims to establish new area-wide standards for the repo markets, with a view to overcoming the separation between different models in the national markets. These new standards could obviously co-exist with other standards and broader conventions for international transactions. In fact, over the last few months the European Central Bank (ECB) has been examining whether this co-existence could affect the integration of money markets. We have come to the conclusion that, in particular owing to the efforts of the sponsors of the different standards, this should not be considered a threat.

Finally, it should also be noted that national and international central securities depositories are currently developing links with one another, which will enable participants in one country to make direct use of securities deposited in other countries. Twenty-six of these links (concerning mainly Belgium, Germany, France, Luxembourg, the Netherlands, Austria and Finland) may be used by the Eurosystem.

Похожие работы

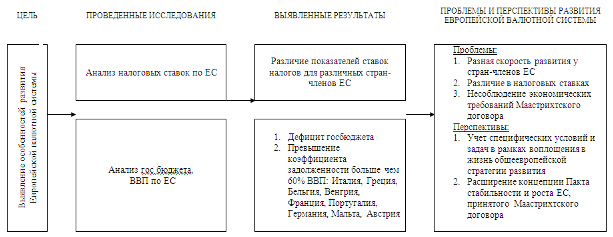

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев