Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

DEALING WITH EUROPEAN UNEMPLOYMENT

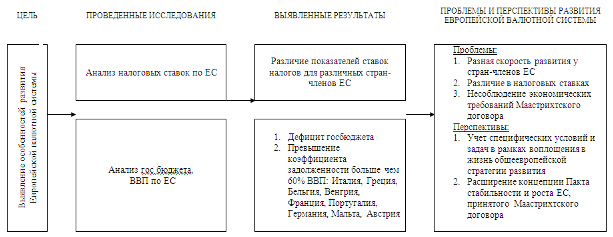

Европейская денежная система

355162

знака

0

таблиц

0

изображений

5. DEALING WITH EUROPEAN UNEMPLOYMENT

The second challenge comes from the high level of unemployment in Europe.

Every economist, observer or policy-maker would probably agree that the most serious problem for the European economy, today and in the years to come, is high unemployment. In large parts of continental Europe the economic system just seems to have lost the ability to create new jobs.

Also on the nature and causes of European unemployment there is a large degree of agreement, as there was agreement on the nature and causes of European inflation well before price stability was finally restored in the 1990s. The key words describing such agreement are structural factors and flexibility. There is agreement that perverse incentives, direct and indirect taxation of labour, unsustainable pension schemes, overly tight employment rules and rigidities throughout the economy are the main obstacles to the creation of new jobs. There is agreement that the typically European welfare state system should be profoundly corrected, but not suppressed. Many also think that rather than following a "Thatcherian" policy of cracking down on the trade unions, it would be preferable to work with, rather than against, the labour organisations, although reform entails occasional confrontations.

As with inflation in the 1970s and 1980s, so unemployment in the 1990s - while being a European disease - is quite diversified across European countries and regions, due to differences in both policies and economic situations. It is over or around 20 per cent in the Mezzogiorno and Sachsen-Anhalt, but below 7 per cent in Lombardy and Baden-Wьrttemberg; over 18 per cent in Spain, but less than 4 in the Netherlands.

Notwithstanding the intergovernmental debates at a European level and the stated intention to undertake common initiatives, the instruments of employment policy remain in national hands, although only partly in the hands of governments. I regard this as appropriate because competition should not be suppressed from the labour market.

Adopting the appropriate policies of structural reform has proved extremely difficult in many key European countries, including my own and this one. Other countries, such as the Netherlands and the United Kingdom, have been more successful. Even the most successful experiences, however, have shown that reducing unemployment is a long and gradual process. Although some countries started labour market reforms in the early 1980s, they only reaped the benefits in the 1990s.

Unemployment will thus remain with us in the years to come and I am convinced that it should be regarded as the greatest policy challenge not only by governments and labour organisations, but by the Eurosystem as well. Let me explain why.

An economy in which unemployment drags above 10 per cent for years is a sick economy, just like one in which public finances or inflation are chronically destroying savings. To operate in a sick economy is always a risk for the central bank and for the successful fulfilment of its primary mission. In the case of prolonged unemployment, the risk arises both on a functional and an institutional ground.

On a functional ground, i.e. from the point of view of the relationship between economic variables that models usually consider, a chronically weak economy is one in which expectations deteriorate, investments stagnate, consumption declines. Structural unemployment may increase the risk of a deflationary spiral because a longer expected duration of unemployment may imply that households respond more conservatively (in terms of increasing savings) in the face of a deflationary shock. Today, we see no signs of deflation. Markets and observers who pay attention to communications by the Eurosystem know that the monetary policy strategy of the euro area is symmetrical, equally attentive to inflation and deflation. Thus, they know that if that risk became reality, the Eurosystem would have to act, and would act. But we know that monetary policy is much less effective in countering deflation than it is in countering inflation.

A more insidious threat, however, may arise on the institutional ground. It comes from a chain of causation involving social attitudes, economic theory and policy, actual economic developments and institutional arrangements. Attitudes of society respond to economic situations and policies, which in turn depend on the state of development of economics. Institutions, on their part, are influenced by attitudes of society. Both the course of economic thought and the practice of policy were lastingly altered by the Great Depression. The epitome of this historical event was the Keynesian revolution. In many countries the strong consensus about the primacy of price stability and the independence of the central bank was the outcome of the prolonged inflation suffered in the 1970s and 1980s. Here in Germany, it is rooted in the experience of hyperinflation. Would such a consensus survive if high unemployment remained a chronic feature of key European economies for many more years? And how would the position of the central bank change if that consensus faltered?

As central bankers primarily concerned with price stability, what can we do to cope with this challenge and to reduce the risks? My answer may seem disappointingly partial, as I do not think there is a miraculous medicine that monetary policy can provide. I would phrase it as follows.

Firstly, the central banker should be aware of the danger. He should know that in the future his principal objective may not receive, from the public, governments and parliaments the same strong support which has been the outcome of the two decades of high inflation. Since unemployment is what concerns the voters and the youngsters most, it may be increasingly necessary for him to play an educational role in explaining the benefits of a stable currency to those who have not directly experienced the costs of inflation. This is very much like the case of the post-war generations in Europe which, being fortunate enough not to experience the horror of World War II, need now to be reminded about the human costs of that terrible conflict.

Secondly, the central banker should avoid mistakes. It may seem obvious, but he should never forget that independence does not mean infallibility and that the likely new environment will offer no forgiveness for mistakes. A mistake would be the attempt to provide a substitute for the lack of structural policies by providing unnecessary monetary stimulus: it is not because the right medicine is neither supplied by the pharmacist nor demanded by the patient that the wrong medicine becomes effective. Another mistake would be to give the impression that the central bank has a ceiling in mind for growth, rather than for inflation. On the contrary, the central bank should make it clear that any rate of non-inflationary growth is welcomed and would be accommodated, the higher the better.

Technically, this will not be an easy task. The analytical uncertainty surrounding estimates of potential output and its growth rate might lead the central banker to respond quite cautiously to evidence of shifts in the rate of non-inflationary growth. While such caution is certainly optimal from an inflation stabilisation point of view, it might be wrongly interpreted as a systematic deflationary bias by the public and the politicians. This is a clear case in which any progress made by scholars in refining the analytical tools of the economic profession will greatly help the central banker to achieve his goals without imposing unnecessary costs on society at large.

On the whole, however, it is part of the central banker's role to make the day-by-day decisions that, in the end, constitute monetary policy. This responsibility can be neither transferred to, nor challenged by, policy makers responsible for other areas. Last week, the Eurosystem has made, for the first time in its life, an affirmative monetary policy decision by lowering its official rates. In this way, the Eurosystem has acted in line with its monetary policy strategy and made a significant contribution towards an economic environment in which the considerable growth potential of the euro area can be exploited in full. It is now the responsibility of other sectors of economic policy making to do their part by strictly adhering to the Stability and Growth Pact and implementing decisive structural reforms.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев