Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

Monetary policy strategy of the ESCB

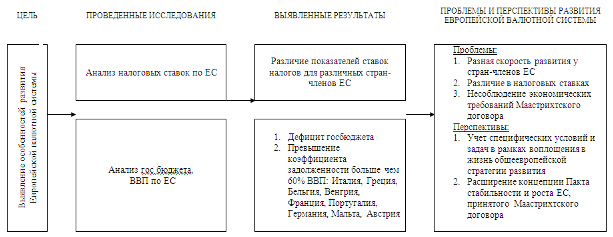

Европейская денежная система

355162

знака

0

таблиц

0

изображений

3. Monetary policy strategy of the ESCB

We are now approaching the start of the Third Stage of EMU. The decision-making bodies of the ECB have made a certain number of important decisions since the ESCB was established. As part of these decisions, the monetary policy strategy of the ESCB was recently announced and explained to the public. The selected stability-oriented strategy promotes as much continuity as possible with the existing strategies of national central banks in the EU. At the same time, its design is adapted to the unique situation of introducing a single currency in eleven countries, which may to a certain extent change economic behaviour. Therefore as much continuity as possible and as much change as required is the thrust of our strategy.

Our strategy consists of two pillars. The first is an important role for money and the second is a broad-based assessment of the outlook for price developments in the euro area. The main reason for assigning a prominent role to money is the empirically well-founded view that inflation, at least in the long run, is a monetary phenomenon. This simple and obvious observation led the Governing Council to announce a quantitative reference value for the growth of a broad measure of money. This choice will create a "nominal anchor" for monetary policy and therefore help stabilise private inflation expectations at longer horizons. The reference value will be derived in a manner that is clearly consistent with - and serves the achievement of - price stability. It will be constructed such that, in the absence of special factors or other distortions, deviations of monetary growth from the reference value will signal risks to price stability.

However, it has to be clear that the reference value is different from an intermediate monetary target, as the ESCB has not made any commitment to correct deviations of actual monetary growth from the reference value over the short term. In particular, it has been realistically recognised that the move to a single currency and ongoing financial innovations may generate fluctuations in the selected monetary aggregate which are not necessarily associated with inflationary or deflationary pressures. For this reason, it is important to continuously monitor the relevance of temporary factors or even structural changes in order to avoid a mechanistic policy reaction to deviations of the chosen monetary aggregate from the reference value. The results of this analysis and its impact on the ESCB's monetary policy decisions will be explained to the public.

Let me turn now to the second key element of the monetary policy strategy, the broad-based assessment of the risks to price stability. The information contained in monetary aggregates, while of the utmost importance, will by no means constitute the whole of the "information set" in the hands of the ESCB. In parallel with the analysis of money growth, a wide range of economic and financial variables will be used to formulate an assessment of the outlook for price developments. The envisaged strategy will enable the ESCB to perform a cross-check between the information coming from the evolution of monetary aggregates and those from other economic and financial indicators.

4. Recent economic developments and prospects

Let me turn to the current economic situation. The euro area experienced a strengthening of economic growth in 1997, to 2.5%, and a further acceleration has been anticipated for this year. The global environment has, of course, deteriorated in the meantime, but this has not so far had an observable impact on growth which has, in any event, been increasingly led by domestic demand. Inflation has remained subdued and even fallen somewhat over the past year, partly as a result of the impact of weaker global demand on oil and commodity prices. However, the favourable pattern of inflation has also been supported by domestic factors, such as a very moderate development in unit labour costs and industrial producer prices.

Concerning recent price developments, HICP inflation for the euro area fell to 1.0% in September, due to a strong impact from food prices, but I would not want to read too much into this latest decline as some price components can be relatively volatile over short periods. More significantly, preliminary data suggest that various broad monetary aggregates for the euro area are increasing at between 3 and 5%, and thus do not appear to signal any strong incipient inflationary or deflationary pressures. We are in line with the consensus view that inflation in the euro area will rise moderately in 1999, but remain below 2%. I do not consider deflation to be a serious risk for price stability at present.

So far, despite the worsening of the global environment, euro area-wide activity has continued to expand at a fairly stable rate. At around 3%, annual real GDP growth was broadly unchanged in the first half of 1998 from the solid growth seen in the second half of 1997. Industrial production growth has slowed somewhat since the spring. More recent evidence, particularly that of the area-wide survey data, may also suggest a moderation in the pace of growth and further developments in these indicators will continue to be monitored closely. Area-wide growth should, however, be supported by a number of domestic factors. One factor supporting continued growth, particularly in private consumption, is the gradual improvement in labour market conditions. Moreover, the lowest short-term interest rates in the euro area currently stand at 3.3%, and several countries have cut interest rates towards this level recently as part of the process towards interest rate convergence. The process of convergence towards this level has been gradual, but should imply a reduction in the average short-term interest rate in the euro area of about 0.5 percentage point since July. Long-term rates also stand at low levels. And, there has been a marked degree of exchange rate stability among countries participating in the euro. This is undoubtedly a welcome development from the standpoint of encouraging trade and investment. Thus, our assessment is similar to that of other international organisations, that - unless the international environment deteriorates further, which is not currently expected - growth will be somewhat weaker in 1999. Growth should, however, remain high enough to support continued employment creation and, assuming a recovery in the international environment, there should be a pick-up in growth in the year 2000. At the meetings in December the ECB Governing Council will again assess the outlook for economic and price developments.

Although the economic outlook may be less favourable than expected - let us say - half a year ago, I believe that the conditions for a successful launch of the euro are in place. You can be sure that the ESCB will do its utmost to make the euro a stable currency.

The euro: pushing the boundaries

Presentation by Ms Sirkka Hдmдlдinen,

Member of the Executive Board of the European Central Bank,

at the symposium arranged by the European Private Equity and

Venture Capital Association

on 11 June 1999 in Prague

It is a great honour for me to be invited here today to this symposium arranged by the European Private Equity and Venture Capital Association to speak about the new European currency - the euro. Indeed, the theme of this symposium - "Pushing the boundaries" - is very appropriate when speaking about the euro. To my mind, the establishment of Economic and Monetary Union can be characterised as pushing the boundaries in several ways, such as:

* pushing the boundaries in the process of European

integration;

* pushing the boundaries of stability-oriented policies in

Europe; and

* pushing the boundaries of market integration in Europe.

In today's presentation, I shall give an overview of these three aspects of Economic and Monetary Union. Thereafter, I shall discuss more thoroughly the implications of the single currency for the development of the European financial markets, focusing on the capital markets. Finally, I shall reflect briefly on the importance of equity prices, and other asset prices, in the formulation of monetary policy.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев