Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

MANAGING FINANCIAL TRANSFORMATIONS

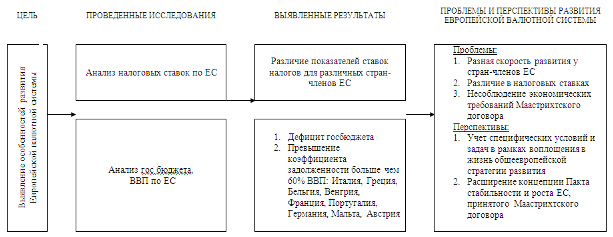

Европейская денежная система

355162

знака

0

таблиц

0

изображений

6. MANAGING FINANCIAL TRANSFORMATIONS

The third challenge consists in accompanying and surveying the rapid changes the European financial institutions and markets are undergoing, and will continue to undergo over the coming years, partly - but not exclusively - as a consequence of the euro.

It is sufficient to observe the US Federal Reserve System to understand the role the Eurosystem should play in the coming years: attention in monitoring changes in the financial system, active participation in the policy debate caused by such change, intense dialogue with both the Administration and Congress, influence exerted on opinions and decisions.

To a large extent the factors of change are technology determined, hence independent of the euro and even not specifically European. Technology is the driving force of the transformation in banking and finance that modifies the traditional deposit loan structure of banks. Technology also reshapes dramatically the back office and the communication with customers, thus producing massive over-branching and over-staffing in traditional banks. Also the globalisation of finance comes primarily from the combination of data processing and telecommunications.

Other changes are specifically European. Since universal banking has historically prevailed in continental Europe, the change from an institution-based to a market-based financial system is particularly significant in this part of the world. Similarly, the development of financial conglomerates is more pronounced in Europe than in the United States or Japan. Typical of continental Europe are also the labour market rigidities that make the restructuring of banks so difficult and slow.

Finally, there are changes induced by the euro. The removal of currency specificity as a cause of national segmentation of the financial industry is causing a convulsive shake-up of both institutions and markets. Since the beginning of this year, about ten banks ranking near the top of their respective national lists have concluded or started merger operations in France, Spain, Italy, the Netherlands, Belgium and Norway. In most European countries stock exchanges and other organised markets, which were legally and structurally organised as providers of a public service, have been transformed into profit-driven private institutions and are now in a process of rapid concentration. In the coming two or three years the number of banks will shrink, the largest banks will become much larger, few financial centres and market networks will replace the present one-country one-centre configuration.

In any national system the central bank would actively monitor and even guide the course of such a transformation. It would do so along with the various agencies responsible for financial supervision and competition policy, and with an involvement of the executive power itself. Although largely determined by business decisions, these developments indeed involve the public interest in various ways.

Surveying and accompanying a profound transformation of the financial industry would be a difficult task for any central bank. For the Eurosystem it will represent a daunting challenge because it will put to the test an unprecedented articulation of the policy functions that are called for. Let me briefly explain this assertion.

The institutional setting of the euro area establishes a double separation between central banking and other public functions. Firstly, a functional separation, whereby banking supervision is now assigned to institutions that - even when they are national central banks - no longer exert independent monetary policy functions. Of this separation we have many previous examples (Germany, Japan, Sweden, now the UK, etc.). Much newer is a second, geographical, separation, whereby - with only the partial exception of competition policy - the area of jurisdiction of central banking does not coincide with the area of jurisdiction of the other public functions involved (banking supervision, regulation of the securities market, etc.).

Experts, including academic people, have so far focused attention on lender-of-last-resort functions and suggested that the new setting would not be able to act effectively in a crisis. I have argued elsewhere why this criticism seems unjustified. Here, I would like to suggest that the real challenge could come, in my opinion, from tensions between the national and the euro area interest in the process of financial transformation.

The process of industry transformation will inevitably involve aspects that have traditionally been considered as sensitive by public authorities: suppression of jobs, location of facilities and headquarters. Financial transformation will also produce a hardening of competition and competition will be, to a considerable extent, one between national financial centers and industries, not only between individual banks or institutions. The propensity to defend national champions may prevail over the pursuit of efficiency. The risk for the Eurosystem to fall in the trap of an improper interplay between the EU and the national dimension of the public interest may become high. Like any central bank, the Eurosystem should be both active and neutral in the great transformation of "its" financial industry. The word "system" that is part of its own name refers, and should apply in practice, to the whole euro area.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев