Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

Introduction

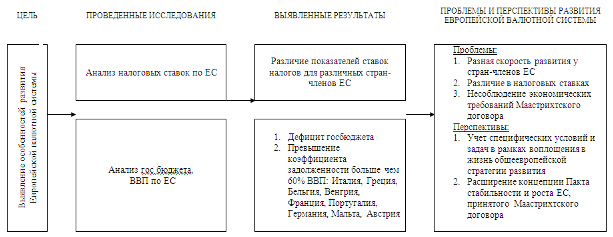

Европейская денежная система

355162

знака

0

таблиц

0

изображений

1. Introduction

Ladies and Gentlemen, I should like to express my appreciation at being invited to deliver a speech at this conference organised by the Royal Institute of International Affairs. It is a great pleasure for me to be here, in London, today.

The topic I am going to address relates to the current position and the future prospects of the European System of Central Banks. I feel that this topic provides me with an opportunity to deal with the objective of the ESCB and its contribution to the other policies in the Community. I will also briefly touch upon the decision-making in the ESCB, recall the main features of our monetary policy strategy and talk about our regard for openness and transparency. The final part of my talk will cover the views of the ESCB on recent economic developments and the future outlook for price stability in the euro area.

2. Independence, transparency and accountability

In the Maastricht Treaty the ESCB has been given an independent status. The reason is that politicians all over the world have come round to the view that monetary policy decisions taken with too close a political involvement tend to take too short a time horizon into consideration. The consequence is that in the longer term such decisions do not support sustainable gains in employment and income, but only lead to higher inflation. This view is confirmed by a host of economic research.

Independence, however, requires a clear mandate. The ESCB has such a mandate. Its primary objective is to maintain price stability. Without prejudice to the objective of price stability the ESCB shall support the general economic policies in the Community. Price stability is not an end in itself: it creates the conditions in which other, higher-order, objectives can be reached. In particular, I share the deep concerns about the unacceptably high level of unemployment in Europe. The ESCB will do what it can to contribute to the solution of this problem. By maintaining price stability inflation expectations and interest rates can be kept at a low level. This creates a stability-oriented environment which fosters sustainable growth, a high level of employment, a fair society and better living standards. Moreover, in specific circumstances, if production, inflation and employment all move in the same direction, monetary policy can play some role in stabilising output and employment growth without endangering price stability. However, the contribution from monetary policy can generally be only limited. Given the structural nature of the unemployment problems the solution is to be found, above all, in structural reforms aimed at well-functioning labour and product markets.

An independent central bank does not only need a clear mandate. It has also to be an open and transparent institution, for at least three reasons. First, transparency enhances the effectiveness of monetary policy by creating the correct expectations on the part of economic agents. A predictable monetary policy contributes to achieving stable prices without significant adjustment costs and with the lowest interest rate possible. The second reason is that in a democratic society the central bank has to account for its policies. Finally, transparency towards the outside world can also structure and discipline the internal debate inside the central bank.

Let me now turn to the ways and means of achieving transparency. As a first element the ESCB has defined a quantitative objective for price stability. It reads as follows: price stability is a year-on-year increase in the Harmonised Index of Consumer Prices (HICP) for the euro area of below 2%. Although I do not consider deflation to be likely in the current environment, I may add that a situation of falling prices would not be consistent with price stability.

The Governing Council has made it clear that "Price stability is to be maintained over the medium term". The ESCB cannot be held accountable for short-run deviations from price stability, for example due to shocks in import prices or specific fiscal measures. A monetary policy reaction to short-run fluctuations in the price level would provide the wrong signals to the market and cause unnecessary interest rate volatility. In summary, the ESCB will react in an appropriate, measured and, when necessary, gradualist manner to economic disturbances that threaten price stability in the medium term, rather than in an abrupt way, in order to avoid unnecessary disruptions of the process of economic growth. That said, the ESCB will, whenever necessary, openly discuss and explain the sources of possible deviations from the quantitative definition of price stability.

In addition, let me remind you that by focusing on the HICP for the euro area, the ESCB makes it clear that it will base its decisions on monetary, economic and financial developments in the euro area as a whole. The single monetary policy has to take a euro area-wide perspective: it will not react to specific regional or national developments.

The institutional implication is that the ESCB should develop into a strong unity, with a strong centre and strong national central banks. It should become a truly European institution, with a truly European outlook. Of course, it may take some time to arrive where we ultimately want to be. We have to get used to thinking in euro area-wide terms. In the ECB Governing Council we are already "practising" that approach and are making progress. I am confident that the ESCB will indeed act as a unity.

Transparency and openness will be apparent from the way in which the ESCB communicates with the public. The ESCB will regularly present its assessment of the monetary, economic and financial situation in the euro area and provide information about each specific monetary policy decision, be it a move in interest rates or an absence of change. This will notably be done by way of press releases, press conferences, publications and speeches. Press releases are made available immediately after the fortnightly meetings of the Governing Council and, as you may know, they always include a precise list of the decisions taken together with background information.

There will be a monthly press conference. Such a press conference will start with a detailed introductory statement, as has been the case so far, and these introductory statements will also be published immediately, without delay. In this statement the Vice-President and I will present the Governing Council's view of the economic situation and the underlying arguments for its monetary policy decisions, followed by a question and answer session.

The publications of the ESCB will include, in particular, an ECB Bulletin each month as well as an Annual Report. As from 1999, a detailed analysis of the economic situation in the euro area will be presented in the monthly Bulletin. Thematic articles in this Bulletin will include in-depth analyses by the ECB on matters regarding the monetary policy of the ESCB and the economy of the euro area. Further, you may also recall that, as required by its Statute, the ESCB will publish its consolidated balance sheet on a weekly basis.

My colleagues on the Executive Board of the ECB and I intend to be very active in giving speeches dealing with all issues of relevance for the conduct of monetary policy. I am convinced that the Governors of the national central banks will also play their role in this respect.

Since I am talking about the communication and external relations of the ESCB, I would like to underline that I am prepared to accept invitations to appear before the European Parliament at least four times a year to present the activities of the ESCB and the ECB's Annual Report. Finally, it should be noted that the ESCB will have a regular exchange of information and views with the ECOFIN. Representatives of the ECB will be invited to ECOFIN meetings whenever issues of concern to monetary policy are discussed. A similar relationship will naturally also exist with the EURO-11, whose meetings will generally be attended by the President of the ECB, whenever matters relevant to the ESCB are on the agenda.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев