Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

The monetary policy strategy

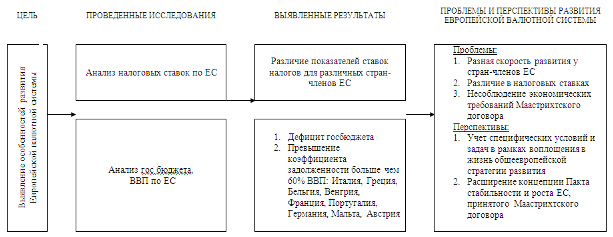

Европейская денежная система

355162

знака

0

таблиц

0

изображений

4. The monetary policy strategy

The ECB has, as I mentioned earlier, such a mandate. However, the Treaty does not specify how the ECB should pursue its primary objective of maintaining price stability; in other words: it is silent on what is called the monetary policy strategy. The ECB therefore formulated its strategy in the second half of last year. That was no easy task. The introduction of the euro constitutes a structural break, which may change the behaviour of firms and individuals and make it less predictable. To a certain extent it is comparable to what Poland experienced when it embarked on its reform process. The rules of the game change and this makes policy-making more complicated. Our monetary policy strategy has taken these specific circumstances into account. It is tailored to this unique period of the introduction of the euro, although it has elements of both monetary targeting and inflation targeting.

In the context of this strategy the ECB has provided a quantitative definition of price stability. Price stability is defined as a year-on-year increase in the harmonised index of consumer prices (HICP) of below 2% for the euro area as a whole. Price stability is to be maintained in the medium term.

The strategy consists of two pillars. The first pillar is a prominent role for money. Ultimately, inflation is a monetary phenomenon. It is in the end result of too much money chasing too few goods. Therefore, we have formulated a reference value for the growth of a broad monetary aggregate, M3, of 4 Ѕ% on an annual basis. Growth of the money stock at this pace would provide the economy with sufficient liquidity for growth in activity in line with trend growth, without inflation. At the end of this year this figure will be reviewed. It should be emphasised that we did not define a target for money growth. The reason for this is the structural break that the introduction of the euro creates. By calling this a reference value, it is made clear that money is one variable which we look at very carefully in order to examine whether inflationary or deflationary pressures are tending to emerge. We do not, however, react mechanistically to changes in money growth.

The formulation of the second pillar is also prompted by the potential changes in economic behaviour on account of the introduction of the euro. It is a broadly based assessment of the outlook for price developments on the basis of an analysis of monetary, financial and economic developments. In this context interest rates, the yield curve, wage developments, public finance, the output gap, surveys of economic sentiment and many other indicators are analysed. Use is also made of forecasts produced by other bodies and internally for inflation and other economic variables.

This brings me to the role of the exchange rate of the euro in our strategy. Since our primary objective is price stability and since the euro area as a whole is a relatively closed economy with an export share of 14% of gross domestic product, we do not have a target for the exchange rate of the euro, for example, against the US dollar. This does not mean, and it is good to underline this once more, that the ECB is indifferent to the external value of the euro or even neglects it. The external value of the euro is one of the indicators we look at in the broadly based assessment of the outlook for price developments. Within that framework, we constantly monitor exchange rate developments, analyse them and shall act on them, if and when this becomes necessary. However, such action will never be mechanistic, nor will it be isolated. The external value of the euro and its development are analysed and considered in the context of other indicators of future price developments. The ECB also tries to assess international confidence in the still very young euro. Of course, the level of international confidence in the euro is not the only factor determining its external value, nor is the exchange rate the only indicator of confidence in the euro. It is, for instance, encouraging to see how the euro has been received on the international money and capital markets. I am sure that an internally stable euro will also strongly underpin international confidence in this currency, as it has for other currencies in the past.

As the currency of a very large area, the issue of the international role of the euro naturally arises. The ECB takes a neutral stance regarding this role. It will neither be stimulated, nor hindered. On the one hand, an international currency has advantages for citizens in the euro area, on the other, it may sometimes complicate the conduct of monetary policy when a large amount of euro is circulating outside the euro area. We shall leave the development of the international role of the euro to market participants and market forces. If history is a guide as to what will happen, there will be a gradual process whereby the euro will have an increasingly international role. Such a gradual development would also be a welcome development, if only to prevent the euro from becoming too strong externally at some point in time. It is likely and understandable that interest in the euro is already considerable in those countries aspiring to join the EU, including Poland. I shall elaborate on this issue at the end of my speech.

Coming back to our monetary policy strategy, I should like to point out that it is important to make clear what monetary policy can and cannot do. Monetary policy can maintain price stability, but only in the medium term. In the short term prices are also influenced by non-monetary developments. Moreover, monetary policy measures only have an impact on prices with long, variable and not entirely predictable time-lags of between 1.5 and 2 years. Therefore, monetary policy-making should have a forward-looking character. Today's inflation is the result of past policy measures, and current policy measures only affect future inflation. The uncertainty of the economic process in a market economy is another reason for policy-makers to be modest. The ECB does not pursue an activist policy. Precise steering of the business cycle or a cyclically-oriented monetary policy are not feasible and are likely to destabilise rather than stabilise the economy. Some commentators have interpreted our recent interest rate reduction as a change to a more cyclically-oriented monetary policy strategy. This is not true. Our strategy was, is and shall remain medium term-oriented and firmly focused on maintaining the price stability which currently prevails in the euro area.

Monetary policy should be supported by sound budgetary policies and wage developments in line with productivity growth and taking into account the objective of price stability. Otherwise, price stability can only be maintained at a high cost in terms of lost output and employment. This also explains why independence should not mean isolation. It is important to have a regular exchange of information and views with other policy-makers. The Maastricht Treaty stipulates that the President of the ECB is invited to meetings of the EU Council meeting in the composition of the Ministers of Economy and Finance whenever there are issues on the agenda which are relevant to the ECB's tasks. The President of the Council of Ministers and a member of the European Commission may attend meetings of the Governing Council, although they do not have the right to vote. The President of the Council of Ministers may submit motions for deliberation. Apart from these formal contacts, there are many informal contacts, for example in the context of the so-called Euro-11 group of finance ministers from the euro area countries. I regularly attend meetings of this group.

Monetary policy cannot be used to solve structural problems, such as the unacceptably high level of unemployment in the euro area. Structural problems call for structural solutions, in this case measures targeted at making labour and product markets work more flexibly. The best contribution the ECB's monetary policy can make in this context is to maintain price stability. In this way one of the conditions for sustainable growth in incomes and employment is created. As important as this is, it should be realised that jobs are created by firms which are confident about the future and not by central banks.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев