Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

MAKING THE EUROSYSTEM A CENTRAL BANK

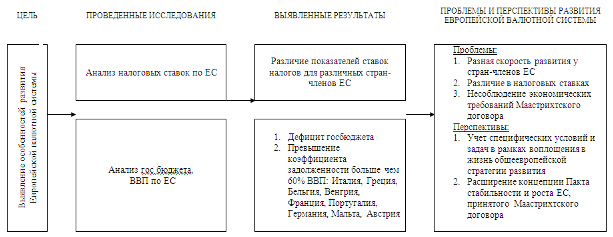

Европейская денежная система

355162

знака

0

таблиц

0

изображений

4. MAKING THE EUROSYSTEM A CENTRAL BANK

The first challenge consists in making the Eurosystem a central bank. It may seem simple, but is not. Let me start my explanation from the two key words of this proposition.

Eurosystem is the word chosen by the ECB to indicate the "ECB+11 participating national central banks", i.e. the central bank of the euro. The Treaty has no name for this key entity, while it refers extensively to the ESCB (European System of Central Banks) formed by the ECB and the 15 European national central banks). However, as long as there are "out" countries, the ESCB in its full composition will remain a scarcely relevant entity because it neither refers to a single currency area nor has any policy competence. Instead, the word Eurosystem indicates clearly the articulated entity which is for the euro what the Federal Reserve System is for the dollar.

Central bank is the institution in charge of the public interests associated with the currency. It originates from fundamental changes in the technology of payments: the adoption of banknotes, cheques and giros, and their final disconnection from gold. These changes have shaped the two other functions that most central banks have derived from the original payment system function: monetary policy and banking supervision. Man-made money made monetary policy possible. Commercial bank money made banking supervision necessary.

These three functions have most often been entrusted to the same institution because they are inextricably linked. Just as money has the interrelated roles of means of payment, unit of account and store of value, so central banking has a triadic function that refers to the three roles of money. Operating and supervising the payment system refers to money as a means of payment; ensuring price stability refers to money as a unit of account and a store of value; pursuing the stability of banks refers to money as a means of payment and a store of value. The function remains triadic (albeit, in my view, in a less satisfactory way) even where prudential control is entrusted to a separate agency. I am referring to the special "supervision" any central bank has over its banking community, necessitated by the fact that banks are the primary creators of money, providers of payment services, managers of the stock of savings and counterparties of central bank operations.

In performing its triadic function the central bank exerts operational and regulatory powers, interacts with other public authorities and the financial community, entertains relations with other central banks, participates in international debates and negotiations about monetary and financial matters. In all these activities it pursues and represents the public interest of a sound currency; all are instrumental to that interest. From the point of view of the perceptions of people and markets all such activities refer to that same public good that we call confidence.

For the Eurosystem the challenge is to rise to a full central banking role as just defined. It is necessary because of the links that bind the various functions of money. The Eurosystem would find it hard to play effectively its most delicate role - the pursuit of a stable currency or, as the German Constitution puts it, "die Wдhrung zu sichern" - if it appeared as an inexplicable exception to the classic paradigm of a central bank. The public, the markets, the international institutions and fora would not understand.

But it is also difficult, because the steps to take are multiple and complex from both a conceptual and a practical point of view. Moreover, they cannot all be taken at once. Let me briefly explain.

In the articulation of any federal constitution (Bund, Land and local, to use the German terminology) the central bank undoubtedly belongs to the level of the "federation", or Bund. The fact that important activities are conducted by "local" components of the system (Landeszentralbanken, or Federal Reserve District Banks) is an organisational feature that does not impinge upon the constitutional position of the central bank. The same happens within Monetary Union. The Eurosystem is the central bank of the euro area, even though operations are carried out - to the extent possible and appropriate - through its component parts, the NCBs. Indeed, the constitutional and the organisational profile of the institution are not in contradiction.

Although a federal and decentralised central bank is not a novelty, the Eurosystem is a special case. It is the central bank of an economy that has a much deeper national segmentation than any other currency area. Its components have for many generations (and until few weeks ago) performed the full range of central banking functions under their own responsibility and in a national context. They have been accountable to, and sometimes dependent on, national institutions. Public opinion has perceived, and still perceives, them as national entities. The notion of the public interest they were referring to was the notion of a national interest. Significant differences existed, and partly remain, in their tasks, organisations, statutes and cultures.

In this situation, making the Eurosystem a central bank requires drawing the appropriate distinction between being national in the organisational sense and being euro area-wide in the definition of the public interest pursued. This is a difficult distinction to draw in conceptual terms, not only in practical terms or from the point of view of personal attitudes.

In the preparatory discussions and negotiations that led to the Maastricht Treaty, central banks took the view that monetary functions are indivisible and that, contrary to the fiscal field, subsidiarity cannot apply to the monetary field. Their traditional and strongly held position has been that the public interest assigned to central bank is a whole which cannot easily be decomposed. Indeed, while there is a fairly well developed theory of fiscal federalism, there is no equivalent for the monetary field.

As I said, I do think that the functions of a central bank constitute a whole that cannot be split. This does not exclude that the Eurosystem should avoid seeking more uniformity than necessary and that some diversity is a positive factor and has always been valued as an aspect of the richness of Europe. Perhaps even a limited degree of internal competition may be used as an incentive to good performance. But can the Eurosystem depart from the two historical models of the Federal Reserve System and the Bundesbank? What are, in conceptual terms, the criteria of what I just called the "appropriate distinction"? What should be the touchstone?

It would be an illusion, I think, to expect or pretend to have a full and satisfactory answer solely from legal interpretation. And it would be unfortunate if the Eurosystem were to fall into the trap of the narrowly legalistic approach that paralyses international organisations. The Eurosystem is not an international organisation, its model is not the Articles of Agreement of the IMF. Of course, the answer will have to comply with the Treaty, which provides useful guidance. However, the system is entrusted to decision-making bodies that are composed not of lawyers, but of central bankers. They carry the primary responsibility to manage the euro and are accountable for that responsibility. They have known for years what a central bank is and how vague the wordings of central bank statutes have historically been. Their touchstone can only be, in the end, the effectiveness in the accomplishment of the basic mission embodied in the triadic paradigm of central banking functions.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев