Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

Bond markets

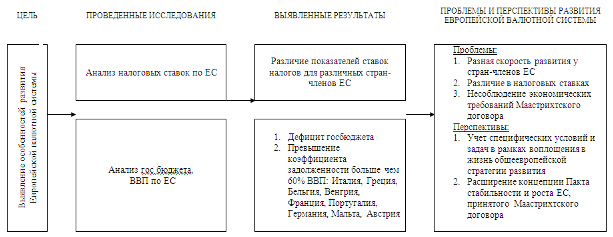

Европейская денежная система

355162

знака

0

таблиц

0

изображений

3. Bond markets

I should now like to turn to bond markets and first to comment on the position of euro area bond markets in the global market. Some data sources on international securities issuance available so far show a pattern of increased reliance on euro-denominated bonds at the beginning of 1999, in particular as opposed to US dollar-denominated bonds. While it remains difficult to draw firm conclusions on the determinants of bond denomination choices without considering information on the nature of bond holdings and trading patterns, recent bond issuance volumes indicate that the euro has the potential to become an important currency for international bond issuance.

The importance of the euro area bond market is also apparent in measures of secondary market activity, i.e. turnover or trading volumes. In particular, trading volumes on exchange-traded bond futures are indicative of the overall degree of market activity. Volumes traded in euro-denominated bond futures were low shortly before the changeover to the euro, when the bond markets in the euro area were exceptionally quiet. Since then, volumes have increased markedly and they currently stand at consistently high levels, which indicates a continuously high degree of turnover in euro-denominated bond markets in general.

Turning to the internal structure of the bond markets of the euro area, I should like to make an initial observation related to the recent marked increase in euro-denominated corporate bond issuance, which was accompanied by an increase in the average size of issues. This tendency is likely to continue in the future, in particular to the extent that bonds may be used by firms to finance increasing mergers and acquisitions activity in the euro area. The underlying reasons for increased bond issuance by euro area firms are clear, both on the supply and on the demand side. On the supply side, large firms with good credit ratings will find opportunities in the increased depth and liquidity of the euro area bond market. On the demand side, the respect by governments of the parameters of the Stability and Growth Pact over the medium term should leave more room for the private sector to issue debt securities. In addition, the euro area must be in a position to save in order to be able to take care of its future pension payments, and a part of these savings is likely to be invested in corporate debt securities. An increase in global demand for euro-denominated debt securities is also expected as the euro becomes a major reserve currency. Moreover, the demand for higher risk euro-denominated debt securities is likely to increase, particularly as the current low level of sovereign yields increases incentives to search for higher yields.

With regard to the government bond markets, an issue of importance for the euro area that I should like to stress is the fact that governments now find themselves in a rather new position as issuers. This reflects a number of developments, two of which I should particularly like to mention. First, the major public issuers have attempted to position themselves as providers of benchmarks for euro-denominated bond markets. Second, certain issues of government bonds have effectively gained larger portions of secondary markets, in particular in relation to developments that have occurred on bond futures markets.

Market participants have responded to these developments in the bond markets with a range of concurring or competing initiatives and alliances. In the derivatives industry, market participants have established new alliances. On the trading side, electronic cross-border platforms for bonds have been created or are in the process of being developed. On the clearing side, integrated platforms for different markets have been launched or are being finalised, while, finally, on the securities settlement side, initiatives have also been launched. It is important to note that while some of these developments are internal to the euro area, others aim at creating links with financial markets outside the euro area. One may reasonably expect that all of these new circuits, as well as others, may in the future be enlarged to encompass a growing number of market participants.

4. Equity markets

Turning to equity markets, structural developments of most interest relate to the infrastructure of stock exchanges on the one hand and equity derivative exchanges on the other. First, within the euro area, equity investment and trading activities appear to be less and less influenced by country-specific factors and increasingly subject to area-wide considerations. Consistent with this development, area-wide equity indices have been developing. Market participants are showing considerable interest in these area-wide indices, in particular as they are also now adopting investment positions on area-wide industrial sectors, using the sub-indices made available for that purpose. An indication of the degree of interest raised by area-wide indices is the relatively fierce competition for benchmark status that has developed between the various proponents of area-wide indices.

Second, market developments in relation to stock index futures and options will reflect the rise of area-wide indices. This may in turn lead to either consolidation or product specialisation of equity derivative exchanges. For my part, I consider the development of fair competition between exchanges to be a positive factor in terms of the improvement of the range of products and services available to the financial industry.

Third, in the equity market the euro has also provided a powerful incentive for the creation of new - and possibly competing - alliances among exchanges. Before the launch of the single currency, circuits had been created for the launch of integrated "new markets" within and beyond the euro area, encompassing the shares of small and medium-sized companies with a high potential for growth. The development in the integration of exchanges has also continued more recently, and, as you know, it has not been limited to the euro area.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев