Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

CONCLUSION

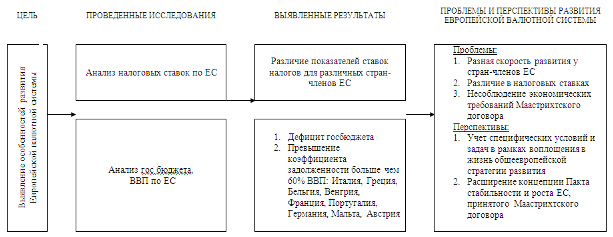

Европейская денежная система

355162

знака

0

таблиц

0

изображений

8. CONCLUSION

I have been fortunate to operate in an environment in which no conflict has arisen between the central banking profession I have exercised for more than thirty years and the European conviction that, like many persons of my generation, I matured in my youth. Since the early '80s I have also been convinced that monetary union, i.e. a confluence of the two motives, was desirable and possible. At the same time, the challenges for the Eurosystem originate precisely from that confluence.

The challenges are not solely economic in their nature, nor can their features be captured by the functional relationships economists are most familiar with. Although partly related to economic factors, their features are in fact tied to the special institutional environment to which the Eurosystem now belongs. They derive from the tension between the completion of the union in the monetary field and the incompleteness of the overall construction. It is a tension because in that environment the notion of the public interest is no longer as simply and statically defined as it was when the Nation-State was an all-pervasive reality and the jurisdiction of the central bank coincided with its jurisdiction. Inevitably, this tension runs through the institutions of the European Union, the Eurosystem itself, and even our minds.

A challenge is a call to a difficult task; it entails the two notions of necessity and difficulty. The problems I have tried to describe are a challenge not only for practitioners, but also for the academic profession, because their solutions can hardly be found in a textbook and will only be invented if the creativity of practitioners will be supplemented with that of scholars.

***

Monetary policy in EMU

Prof. Otmar Issing

Member of the executive board of the European Central Bank

Washington, D.C.

6 October 1998

1. Introduction

On 1 January 1999, the curtain will rise on a world premiиre. For the first time in history, sovereign states will abandon their own currencies in favour of a common currency, and transfer their monetary policy sovereignty to a newly created supranational institution. This process is all the more unusual from a historical perspective because the national currencies involved are not being abolished because of their weakness. On the contrary, proof of a large measure of monetary stability is demanded as a precondition for participation.

The decision has been taken. The Euro will start on time. It must not - and it will not - fail. The European System of Central Banks (ESCB) will devote its best endeavours to making European Monetary Union (EMU) a success.

The French president recently called this unique project a "great collective adventure". As a central banker I am generally not in favour of "adventures" - but who would deny that there are risks and uncertainties in this enterprise? You should be reassured that at the European Central Bank (ECB), we have the necessary independence, instruments and tools to deal with these risks and uncertainties in a successful way. I will discuss some of these in a moment.

Moreover, when considering the uncertainties implied by the transition to Stage Three of EMU, we should not forget that Monetary Union will also reduce, or even eliminate, a number of risks. This has already been demonstrated, even before the actual introduction of the euro. Recent turmoil in international financial markets did not cause any significant disruption to exchange rates among currencies of the designated participants in Stage Three. This is a clear demonstration of the success of the EMU process.

Today, I will address the role of monetary policy in EMU.

First, I will make reference to the final goal of monetary policy - the maintenance of price stability.

Second, I will discuss some important issues relating to the design and implementation of the monetary policy strategy at the outset of Stage Three of Monetary Union; and

Finally, I will describe some features of the operational framework of the ESCB that have recently been finalised.

Let me begin by discussing the over-riding priority we attach to the maintenance of price stability.

2. The priority of price stability

The Treaty on European Union - the Maastricht Treaty - stipulates that the "primary objective of the ESCB shall be to maintain price stability". It was left to the ESCB to provide a quantitative definition of this primary objective. At the ECB's precursor, the European Monetary Institute (EMI), it was agreed that, in the interests of transparency and accountability, the ESCB's chosen operational definition of price stability should be announced publicly. This announcement would form an important element of the overall monetary policy strategy. Simply defining price stability leaves open the question of why price stability is desirable. As a central banker, the benefits of price stability appear self-evident. Any single argument in favour of price stability cannot comprehensively describe the benefits that it brings.

For instance, concerning the United States, Martin Feldstein has recently shown that, in combination with taxes and social contributions, even quite modest rates of inflation can cause considerable real economic losses. Research at the Bundesbank has produced similar results for Germany.

But elimination of the losses caused by this channel is only one illustrative example among the many benefits of price stability. The greatest contribution that the ESCB can make to the euro area's output and employment performance is to achieve and maintain the stability of prices. Stable prices are at the core of the 'stability culture' we are trying to create in Europe, a culture that is the foundation of sustainable and strong growth in the standard of living for Europe's citizens.

At the same time, the ESCB does not operate in a vacuum. Monetary policy needs to be supported by an appropriate fiscal policy and necessary structural reforms implemented at the national level if this 'stability culture' is to be built on solid and sustainable foundations. The private sector also has its part to play, notably by exercising wage moderation, given the high levels of structural unemployment in the euro area. Progress on all these dimensions is not only desirable, but also absolutely necessary. Monetary policy alone cannot ensure strong, non-inflationary growth and improved employment prospects throughout the euro area. However, only a monetary policy focussed closely on the achievement of price stability can lay the basis for these conditions.

Of course, that is not to say that the ESCB can, or should, ignore broader macroeconomic considerations. For instance, the threats posed by deflation in combination with nominal rigidities to the real economy have to be taken into account. In order to prevent any misunderstanding, let me be very clear: my discussion of deflation has to be seen in the context of the formulation of an optimal definition of price stability for the ESCB that takes into account deflationary dangers. These dangers certainly cannot be ruled out and our definition of price stability should reflect them. However, simply recalling the current rate of inflation in the euro area - 1.2% - shows that deflation is not an immediate concern for policy-makers.

While periodic and transitory falls in the price level may be normal, and should not give rise to major concerns, a prolonged deflation is clearly inconsistent with any meaningful definition of price stability. Moreover, since nominal interest rates cannot fall below zero, a prolonged deflation may render the interest rate policy of the central bank rather ineffective. What remains is out-right purchases of assets - both foreign and domestic.

Similarly, the ESCB cannot ignore the implications of nominal rigidities in wages and prices for the transmission mechanism of monetary policy. If we were to live long enough under a regime of stable prices, I would not exclude the possibility that wage and price setting behaviour would adapt, and nominal rigidities would finally disappear. This would reduce some of the potential output costs of fighting inflation, and thus increase the net long-run benefits of price stability. However, for the time being we may have to live with these rigidities and take their effects into account when deciding on our monetary policy strategy.

In this respect, the present situation is not easy for the ESCB. Unemployment in the euro area is currently very high.

However, in contrast to these persistently high levels of unemployment - which are largely structural in origin - the prospects for maintaining price stability are currently very encouraging. Inflation expectations and long-term interest rates in the euro area are at close to historical lows. Actual area-wide inflation is also very subdued.

The current low 'headline' rate of inflation has been moderated somewhat by recent falls in oil and commodity prices, themselves stemming, in part, from the economic and financial crises in Asia and, more recently, in Russia. However, this effect on inflation has been largely off-set by the impact of indirect tax rises in a number of participating countries, which have raised consumer prices for certain goods. All in all, the changed external environment contributes to an overall outlook of very subdued inflationary pressures.

In defining price stability, one might ideally refer to a conceptual measure of 'core' inflation that tries to isolate monetary effects on the price level - for which the ESCB is properly responsible - from such terms of trade or indirect tax shocks, over which it has little immediate control.

In our month-to-month communication with the public, 'core' measures of inflation may prove useful. But, in its preparatory work for Monetary Union, the EMI recognised that any sensible definition of price stability for the euro area would have to be based on a comprehensive and harmonised price measure. 'Core' measures of inflation typically exclude some items. They are unlikely to be comprehensive enough to satisfy the requirements of an index suitable for a sensible public definition. These considerations point to using the 'headline' measure of the harmonised index of consumer prices (or HICP) for the euro area in the definition of price stability.

Finally, the ESCB needs to build on the success of its constituent national central banks (NCBs) in reducing inflation and achieving price stability during the convergence process in Stage Two of EMU. Given the current generally benign inflation outlook in the euro area that is the product of these accomplishments, there is an understandable desire to 'lock-in' the current success in achieving price stability as well as the apparent credibility of monetary policy, and ensure continuity with existing central bank practice.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев