Bond markets

Banking

POLICY MISSIONS

MAKING THE EUROSYSTEM A CENTRAL BANK

DEALING WITH EUROPEAN UNEMPLOYMENT

MANAGING FINANCIAL TRANSFORMATIONS

COPING WITH A LACK OF POLITICAL UNION

CONCLUSION

The importance of the monetary strategy for a successful start of European monetary policy

The new monetary policy instruments and procedures for the euro area

Minimum reserve system

Introduction

Monetary policy strategy of the ESCB

Pushing the boundaries of the process of European integration

Pushing the boundaries of stability-oriented economic policies

Pushing the boundaries in the development of financial markets

The Eurosystem and the equity markets

Introduction

The monetary policy strategy

Accountability and transparency

Навигация

Introduction

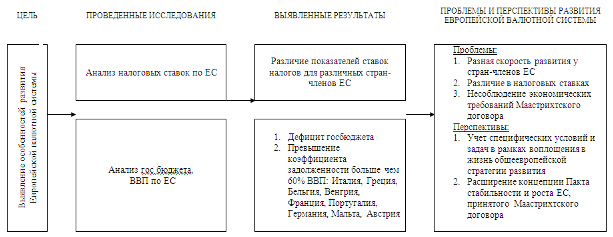

Европейская денежная система

355162

знака

0

таблиц

0

изображений

1. Introduction

First and foremost, I should like to congratulate the National Bank of Poland (the NBP) on its 75th anniversary. The age of the NBP already suggests that as the President of the European Central Bank (ECB), an institution that is even less than one year old and has only been conducting monetary policy since January this year, I should be modest. I am aware that the role of the NBP has not been constant over these 75 years and that in the past decade, in particular, the NBP has gone through a remarkable restructuring process. My previous central bank, de Nederlandsche Bank, has, together with the International Monetary Fund and many national central banks, been involved in assisting the NBP in its efforts to adapt to the role of a central bank in a market economy. Of course, the real work had to be done by you yourselves and I believe you can be proud of what has been achieved over the past decade.

Today in my speech I should like to focus on the role of the ECB, as a truly European institution. First of all, I shall explain the background against which the introduction of the euro and the establishment of the ECB should be considered. Thereafter, I shall discuss the main features of the institutional structure that determines monetary policy-making. I shall then turn to our monetary policy strategy and the role of accountability and transparency in this strategy. I shall conclude by briefly addressing the issue of EU enlargement.

2. The process of European integration

On 1 January of this year the euro was introduced in 11 countries with a combined population of almost 300 million. The ECB started to conduct a single monetary policy for the so-called euro area. Former national currencies, such as the French franc and the German Mark are no longer autonomous currencies, but subdivisions of the euro. Euro banknotes and coins will only be introduced in 2002.

The voluntary transfer of monetary sovereignty from the national to the European level is unique in history. However, it should not be seen as a single, isolated event. The introduction of the euro is part of the process of European integration. This process started shortly after the second World War and has now been under way for more than half a century. The aims of European integration are not only, or even primarily, economic. Indeed, this process has been driven and continues to be driven by the political conviction that an integrated Europe will be safer, more stable and more prosperous than a fragmented Europe. It is true that economic integration has been the main engine of this process and that, although it has had its ups and downs, integration has delivered important economic benefits. On balance it has been successful.

The introduction of the euro and the establishment of the ECB are important new steps in this process of European integration. They are not the completion of this process, for at least two reasons. First, the launch of the euro can be compared to the launch of a rocket. A good launch is crucial, but only the beginning of the mission. The euro has been launched successfully. The challenge now is to make it a success. This will not happen automatically, but will require effort on the part of many authorities, institutions and people. Second, four EU Member States have not (yet) introduced the euro. I hope that this will happen in the future. Moreover, as you are aware, the EU itself is likely to increase its membership over time, also to include Poland. Ultimately, this is bound to extend the euro area. This process, too, is already requiring and will continue to require great efforts: no pain, no gain, as is often the case.

3. The institutional framework of the single monetary policy

Let me now turn to the institutional framework for the conduct of the single monetary policy. This was laid down in the Treaty establishing the European Community, the so-called Maastricht Treaty, and the Statute of the ESCB, which is an integral part of this Treaty. According to the Treaty the ECB has the primary objective of maintaining price stability. Without prejudice to this objective, it is to support the general economic policies in the Community, with objectives such as economic growth and high employment.

Decisions on monetary policy are made by the Governing Council of the ECB. This body comprises the six executive directors of the ECB and the 11 governors of the national central banks (NCBs) of the Member States which have introduced the euro. These 17 people meet every fortnight at the ECB, in Frankfurt am Main. Decision-making on monetary policy is fully centralised. All members of the Governing Council have one vote, whether they come from Germany or Luxembourg. This is because of an important principle. They are not representing their country, but are obliged to take decisions on the basis of euro area-wide considerations. Regional or national monetary policy does not and cannot exist in the euro area. There is only one, single monetary policy for the euro area as a whole. Therefore, the ECB should develop into a truly European institution. This is a process that will inevitably take some time, but my feeling is that we are already making good progress.

The execution of monetary policy is to a great extent decentralised. It is in large part carried out by the NCBs. The ECB and the 11 NCBs together are referred to as the Eurosystem. If we refer to the ECB and the 15 NCBs of all EU Member States, we speak of the European System of Central Banks (ESCB). The General Council of the ECB meets quarterly and comprises the President and Vice-President of the ECB and the 15 governors of the NCBs of all the EU Member States. This body does not make decisions on monetary policy, but discusses issues concerning the relationship between the "ins" and the countries I prefer to call "pre-ins", such as exchange rate issues. The third decision-making body of the ECB is the Executive Board of the ECB, comprising the six executive directors of the ECB. The Executive Board is responsible for current business and the implementation of monetary policy as decided by the Governing Council. The staff of the ECB will, in the course of this year, reach a level of between 750 and 800 and is likely to grow further in the years ahead.

The ECB is one of the most, if not the most, independent central bank in the world. Its independence and that of the participating national central banks are firmly enshrined in the Maastricht Treaty. Members of the Governing Council are not allowed to take or seek instructions from anybody, politicians included. Politicians are not allowed to give such instructions. Members of the Governing Council have a term of office of at least five years. The ECB is financially independent.

The independent status of the ECB fits into the recent world-wide trend of granting independence to central banks. This tendency is evidenced by both practical experience and academic research. By shielding monetary policy decisions from political interference, price stability can be maintained without having to give up economic growth. Indeed, in that sense having an independent central bank is a good thing for all concerned. The reason for central bank independence is that monetary policy-making under the influence of politicians tends to focus too much on short-term considerations. This can easily lead to temporary, non-sustainable increases in growth, but inevitably results in lasting increases in inflation with no lasting gains in growth and employment at all. Politicians all over the world have come to realise this and have decided to remove the temptation to pursue short-term gains and to make their central bank independent. It should be underlined that granting this independence is, as it should be, a political decision. An independent central bank needs a clear legal mandate.

Похожие работы

... путей сотрудничества стран Е.Э.С. - задача первостепенной важности на пороге двадцать первого века. . - 18 - 3II. Вопросы финансовой политики Е.Э.С. 22.1. Европейский бюджет. Европейский бюджет не перестает быть в центре внимания финансовых и экономических противоречий между странами-участницами. Такое положение ...

... " не смогли утвердиться. Необходимо было немедленно найти иной вариант реализации европейской валютной системы, который бы уравновесил национальные и интеграционные интересы государств. 4. Европейская валютная система: первый шаг к истинной валютной интеграции. Инициаторами создания ЕВС были канцлер ФРГ Гельмут Шмидт и президент Франции Валери Жирак д'Эстена, которые представили эту идею ...

... 9. Евростат // Дефицит бюджета в еврозоне (данные 2008 года) // Режим доступа [http://ec.europa.eu/eurostat] 10. Сайт Европа. История денежно-кредитного сотрудничества (Европейская валютная система) // Режим доступа [http://europa.eu]; 11. Фонд экономического развития «Центр Экономикс». Европейский фонд межгосударственного валютного регулирования. Выбор режима валютного курса // Режим доступа ...

... США заставляют правительство Канады пристально следить за развитием событий на мировых валютных рынках. Начиная с 80-х гг. важнейшей целью валютной политики Канады была стабилизация обменного курса канадского доллара по отношению к доллару США. ДЕНЕЖНАЯ СИСТЕМА ИТАЛИИ.Денежная единица и денежное обращение. Денежная система Италии за свое многовековое существование ...

0 комментариев